Private sector takes the lead in India’s post-pandemic investment revival

India’s investment momentum remains robust despite global uncertainties, with private sector participation rising sharply and sectors such as power, renewables, data centres, AI and transport attracting the bulk of new capital commitments.

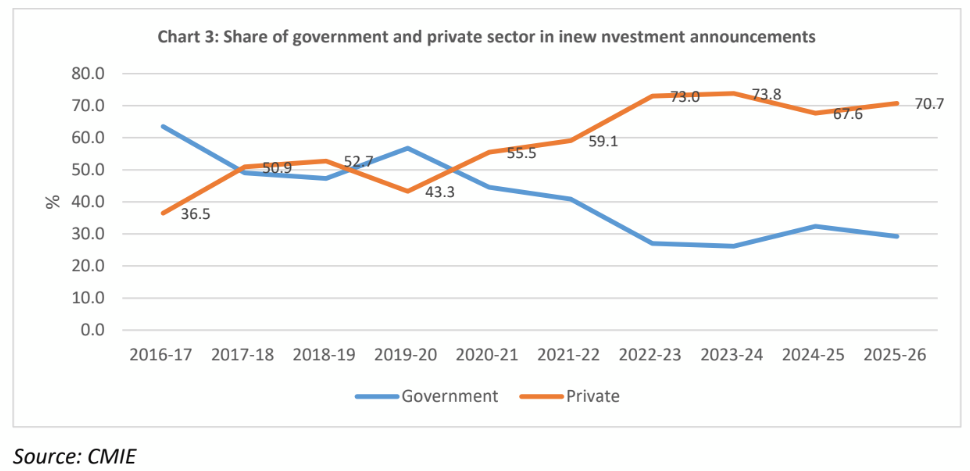

Post Covid, the private sector has had the dominant share of 71.3% between 2022-23 to 2025-26. (AI Image)

There has been renewed push being given to investment post Covid to accelerate growth. The period has been fairly turbulent even after 2021-22 with there being two major wars fought one of which may be coming close to an end. Further, there was a major disruption caused by the imposition of tariffs last year by the government of USA which also added to uncertainty. Given the fact that Indian economy is primarily dominated by domestic demand, there was some bit of insulation. However, inflation has been varied in the last 4 years prompting differential approaches by the MPC which first raised the repo rate before lowering it last year. At the same time there has been an uptick in funds raised in both the IPO and debt market which is encouraging. In this environment the investment pattern in the economy is interesting to examine, according to a research note from Bank of Baroda Economics Research.

Investment is dependent on various factors on both the demand and supply sides. On the demand side, the capacity utilization rate is important because as long as there is excess capacity the decision to invest will be determined by conjectures on future demand. Demand has been varied across sectors with the consumer goods segment being relatively less vibrant against capital goods where there was frontend spending on infrastructure by the government and private sector. On the supply side, cost of capital is also important as companies normally leverage to add to capital and the interest rate becomes important. In parallel, there has been a lot of effort put in at the policy level to ease the doing business environment.

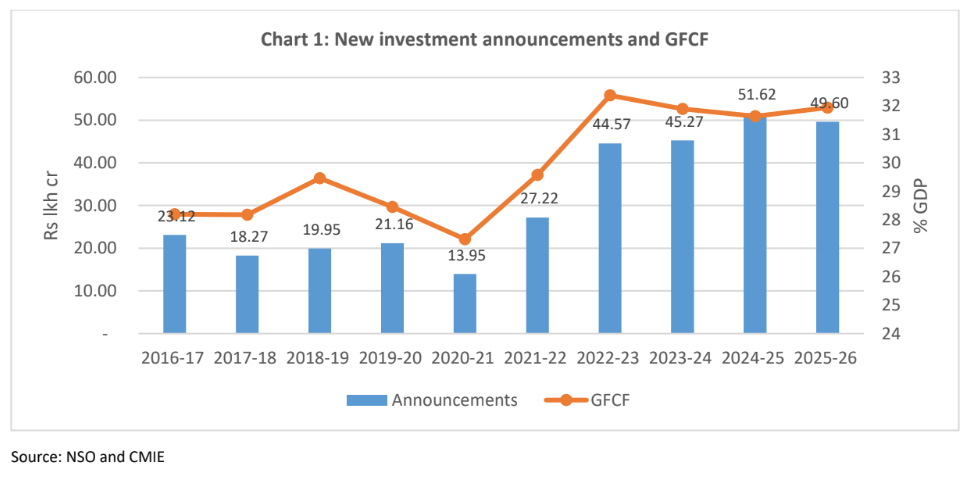

There are two aspects of investment that can be captured by various data sets. The first is the gross fixed capital formation rate (GFCF)which includes construction and investment in plant and machinery and the second is new investment announcements by companies as collated by CMIE. The chart below provides the trend in both these variables over the last 10 years. The GFCF rates are as per 2011-12 base till 2021-22 after which the 2022-23 base year data is used. The new investment announcements are in monetary terms. There is a strong correlation between the two series which also comes out in the graph.

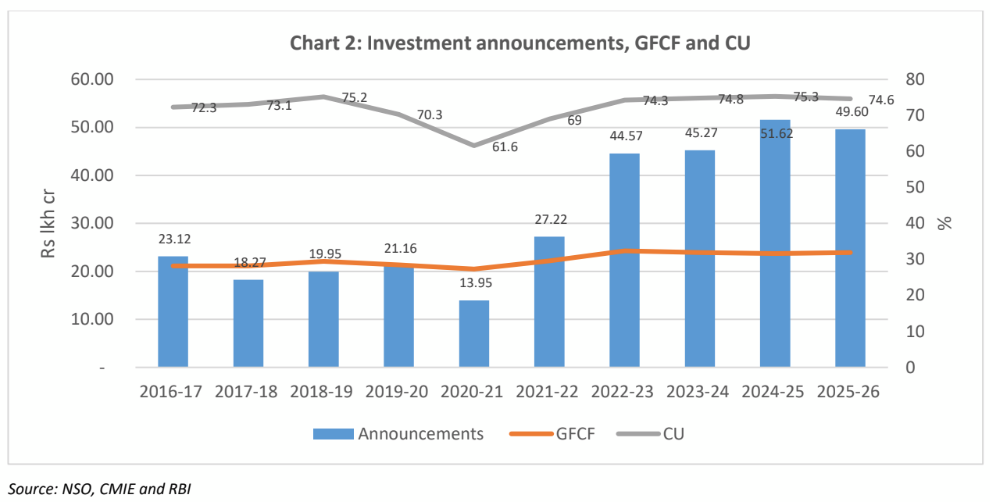

The chart below maps the new investment announcements with the GFCF rates as well as capacity utilization rates of manufacturing sector as presented by RBI. It can be seen that the investment intentions have been showing traction as capacity utilization levels rose post covid and stabilized in the region of 74-75% (though announcements include all sectors while capacity utilization is of only manufacturing companies).

Now, there has been a view that the private sector has a long way to go in investing and this can be analyzed by looking at the share of the government and private sector in total investment announcements over the last 10 years. As can be seen in Chart 3 below, there are interesting findings.

Until covid, the share of the government in total announcements tended to be higher and averaged 54.2% for the 4 years just before covid. Post covid however, the private sector has had the dominant share of 71.3% between 2022-23 to 2025-26. Therefore, there are signs of private sector intentions being in the right direction. In this context, the direction of investment can be looked at next.

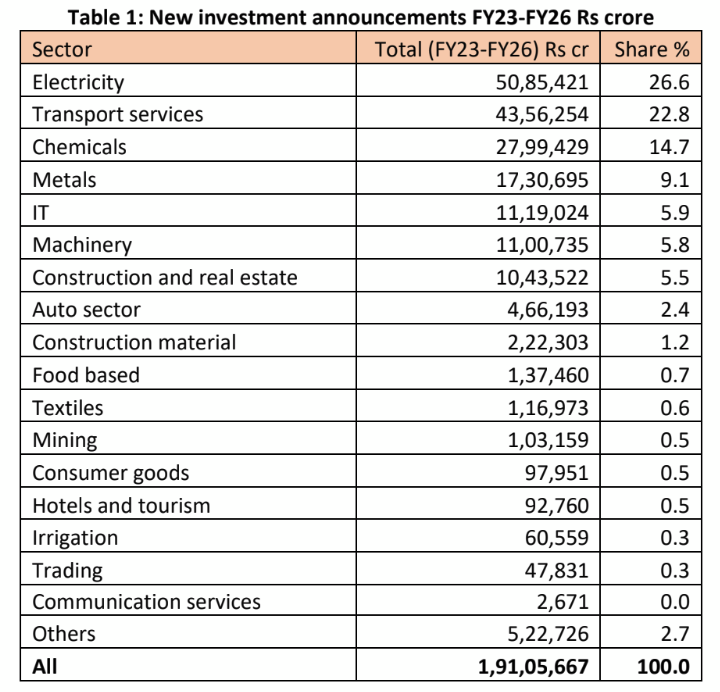

Table 1 below gives the shares of various sectors in cumulative total new investment announcements

between FY23 and FY26. This would be a better indicator than a single year. There are interesting

observations here.

For the 4 years, the total amount of new investment announcements were for around Rs 191 lakh crore which is around Rs 48 lakh crore on an average annual basis. The two dominant sectors which accounted for almost 50% of the total planned investments are electricity and transport services. This is significant as there is a thrust to power generation given the growing requirement which is in both conventional and renewable spaces. In case of transport services, this includes both the plans of the aviation and railway sectors which are on an expansion mode. Two of the airlines had announced plans to purchase new aircrafts which has added to these numbers. Chemicals and metals follow next with a share of around 24%. This gets linked more to infrastructure activity as well as machinery and construction material.

The interesting part is the investment planned in the IT space. With a lot of focus on AI and data centres, there has been progressively higher outlays in these areas. The share is nearly 6% of total.

Now, in the consumer segment, it is only automobiles which have witnessed a share of 2.4% coming in the pecking order followed by food based at 10th with share of 0.7%. Textiles and consumer goods come next with shares of 0.6% and 0.5%. Hence, while the shares are low, there are still investment plans for these sectors.

Hotels and trading have shares of 0.5% and 0.3% which are rising businesses in the last few years.

There has been a change in the consumer mindset where there is higher spending on services (which also comes out in the GDP data) relative to goods which includes both tourism as well as ecommerce.

The investment required here is lower than that in the heavy industries like power or metals and hence have a lower share in relative terms.

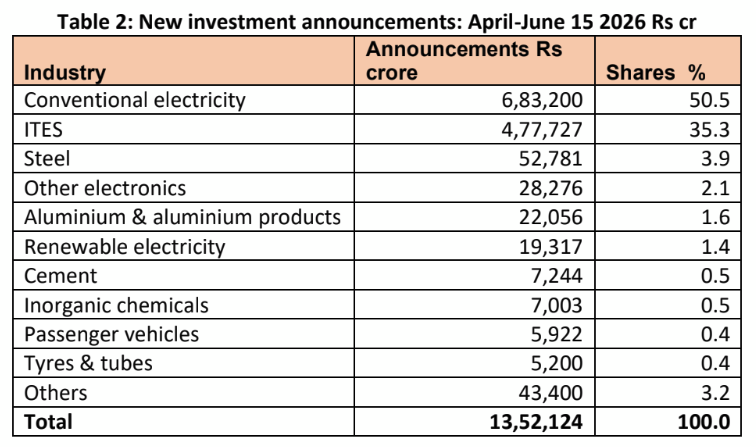

Table 2 below provides information on how these announcements have been made in the first 75 days of the year i.e. up to June 15th. The pattern appears to be similar with electricity and IT dominating and accounting for 85% of total proposed investment. Within the IT space, data centres and AI technology are the main headings for investment.

Concluding remarks

Therefore, the investment environment does appear to be encouraging based on the trends seen in the last four years which persists even during the present financial year. It is natural that there would be certain sectors that will be investing more given the overall demand conditions. Power and IT will however continue to be the dominant industries in the near future as the world turns more to technology areas which will be dominating the economic landscape. Within IT the push given to digital infrastructure as well as data centres will present many opportunities to potential investors. The same holds for renewables which will continue to see traction.