Credit growth pegged at 10–12%, faster than deposit growth: Brickwork Ratings

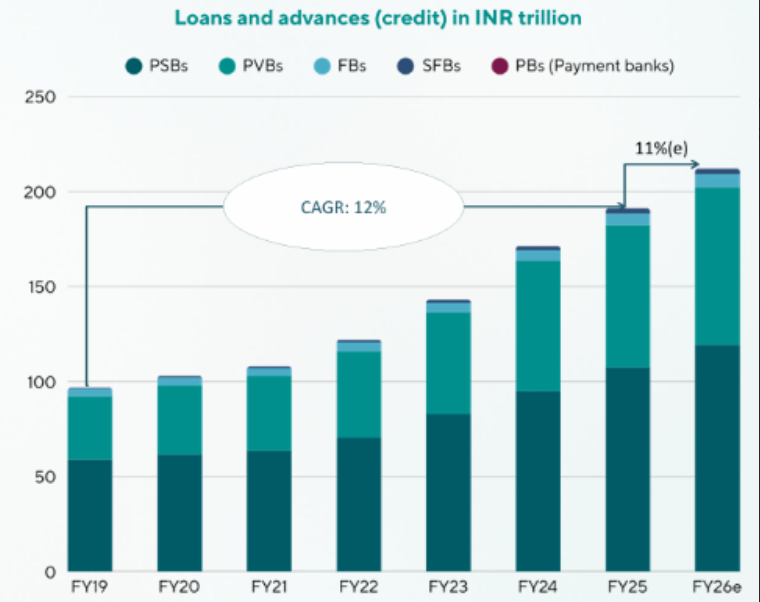

The report pegs credit growth at ~10–12% CAGR over the next five years with the expectation of continued deepening of banking assets as a share of GDP.

Credit to deposit ratios are likely to remain in the high 70s to low 80s range unless a major structural shift occurs. (Image: Freepik)

The asset quality of Indian banks has improved markedly with gross NPAs (GNPAs) falling to multi year lows around 2.2% in September 2025. The capital adequacy ratio (CRAR) of scheduled commercial banks (SCBs) remained strong. Banks maintained strong capital buffers with CRAR around 17.2% as of September 2025, well above the regulatory minimum of 11.5%, according to a recent study on the banking sector by Brickwork Ratings, a leading Indian credit rating agency.

The report pegs credit growth at ~10–12% CAGR over the next five years with the expectation of continued deepening of banking assets as a share of GDP. Retail, MSME and services are key drivers of credit, with housing, vehicle/consumer, and cash-flow-backed SME lending leading growth. “Corporate credit growth is expected to be driven by government capex in private investment, and fresh borrowing, especially in infrastructure, renewables, urban real estate and select manufacturing,” says Manu Sehgal, CEO, Brickwork Ratings.

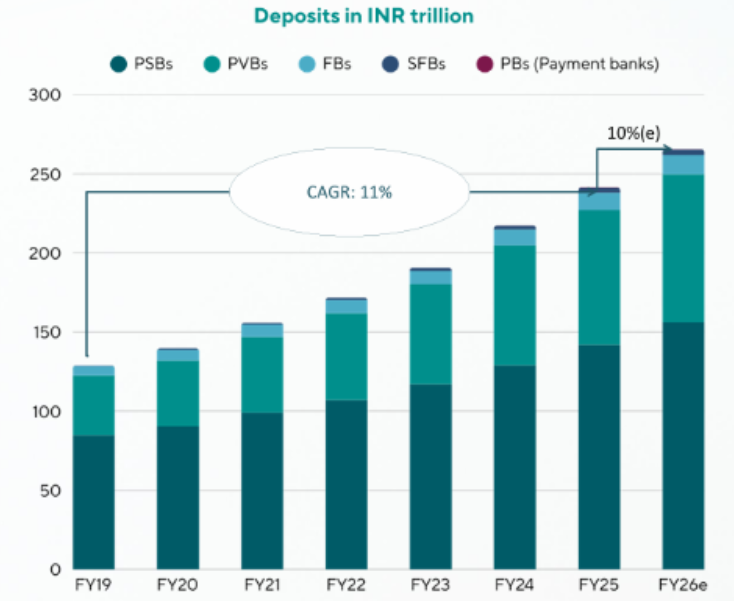

On the other hand, deposit growth is projected at ~9-11% CAGR over the next five years, broadly tracking nominal GDP and credit expansion while remaining below the high-teens growth seen in earlier years. Credit to deposit ratios are likely to remain in the high 70s to low 80s range unless a major structural shift occurs. System level CASA ratios have remained in the high 30s range, but the mix is likely to gradually tilt further towards term deposits, pressuring funding costs and net interest margins unless banks ramp up fee income and operating efficiency.

On the broader banking sector, Hemant Sagare, Director – Ratings, Brickwork Ratings says “Overall outlook for the banking sector is stable to positive, with India’s banking sector well-capitalized to navigate growth, shocks and Basel IV transitions with minimal systemic infusions, whenever required. Potential risks include higher risk-weighted assets from unsecured retail exposure or regulatory changes such as revised risk weights, but strong capital reserves and profitability provide buffers.”

Credit rating outlook robust

“The credit rating outlook remains stable to positive, supported by strong capitalisation and controlled asset quality. CRAR is expected to stay above 16 percent, while GNPA ratios are projected to remain within stress-test thresholds,” says Sagare. Regulatory measures effective by FY26, including risk weight normalization and PSL changes, should aid credit growth. Despite global macro and liquidity risks, capital buffers and policy support underpin rating stability.

Challenges ahead

The banking sector faces rising risks from intensifying competition, tighter regulation, and global shocks. India’s nearly 50 percent share of global digital transactions heightens cybersecurity exposure.

“Aggressive expansion by private banks, fintechs, and big-tech firms is raising customer expectations across retail and SME segments. Meanwhile, stricter Basel norms and digital lending rules are driving up compliance costs. As deposit repricing lags and credit growth outpaces deposits, NIM is expected to dip 10-15 basis points in FY26 and stabilize in the low-3% range from FY27, while macro and liquidity volatility remain key risks,” concludes Sagare.