India’s GDP growth seen at 7.6% as manufacturing, services power Q3 surge

For the full year, GDP growth is estimated at 7.6%, supported by robust expansion in the manufacturing sector.

There has been reasonable traction in consumption demand amidst the recent rationalisation of GST rates. A recovery in urban consumption bodes well for the growth outlook. (Image: Freepik)

India’s GDP growth was recorded at 7.8% in Q3FY26, following a 7.4% growth in Q3FY25. For the full year, growth is estimated at 7.6%, supported by robust expansion in the manufacturing sector. The estimates have been revised upwards from the previous estimate of 7.4% to align with the new base year (2022-23). With respect to the revision, major changes that have been incorporated include double deflation in agriculture and manufacturing in order to capture price issues appropriately, according to a report by the Bank of Baroda.

Going forward, growth is expected to advance in Q4 further as has been evident from the high-frequency indicators. This will be supported by a strong boost to consumption spending along with a revival in investment, as well as accommodative monetary conditions and benign inflation, this bodes well for the growth outlook. Given the rebasing of the GDP series, we do not expect much bearing on fiscal ratios. Overall, we stick with our estimate of GDP growth of 7-7.5% for FY27.

Q3FY26 GDP improves

GDP growth in Q3FY26 accelerates to 7.8% from 7.4% in Q3FY25 on a YoY basis. On expenditure side, higher pace of growth was driven by PFCE with a growth of 8.7% in Q3FY26 against 6% in Q3FY25.

Strength was also noted in investment with GFCE growth of 7.8% compared with 6.3% growth in Q3FY25.Imports growth rose to 8.6% growth in Q3FY26 from 2.9% growth clocked in the previous year of the same quarter. On the other hand, moderation was noted in government spending with 4.7% growth against 7.6% growth previously. Moreover, given the uncertainty on the tariff front during the same period, exports growth eased to 5.6% from 10.5% growth noted in Q3FY25.

On the nominal side, barring imports and investment, broad-based moderation was noted across all the components. Private and government spending was marginally down with 8.9% (from 10.8%) and 9% (from 12.6%) growth in Q3FY26 respectively. Exports growth continues to clock double digit growth albeit at a tad slower pace of 10.3% against 11.3% in Q3FY25. On the brighter side, investment growth with over 30% share inched up by 9% in Q3 compared with 8.8% growth in Q3FY25. Imports growth an increase of 13.4% growth against 9.9% growth for the same period of last year.

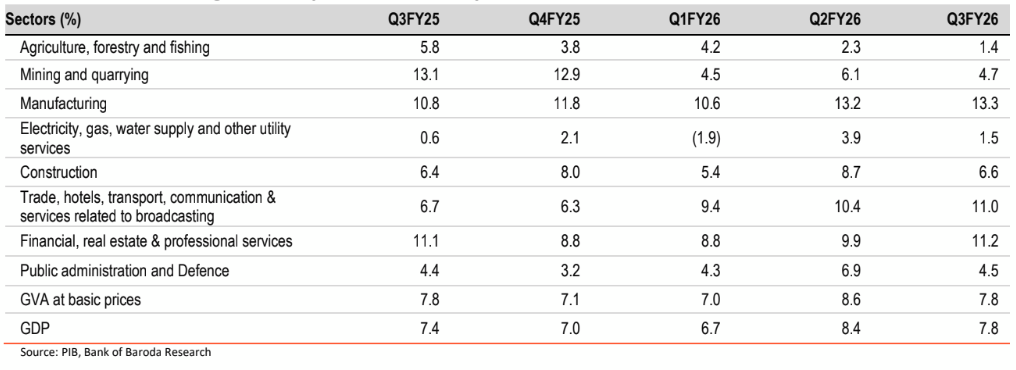

GVA maintains momentum

GVA registered a growth of 7.8% in Q3FY26, up from Q3FY25 (7.4%) as per the new series. Amongst the sectors, major momentum was delivered by both services and manufacturing. Within services, growth was broad based, with trade, hotels noting a growth of 11% in Q3FY26 versus 6.7% in Q3FY25.

Public admin and defence (4.5% versus 4.4%) and financial sector growth continue to rise at steady pace (11.2% versus 11.1%). On the industrial side, manufacturing sector showed resilience as it registered 13.3% growth compared with 10.8% last year during the same period, helped by improvement in corporate profitability. Growth in utilities segment was up by 1.5% from 0.6%, and construction sector recorded 6.6% increase versus 6.4% in Q3FY25. In contrast, agriculture (1.4% versus 5.8%) and mining (4.7% versus 13.1%) sector growth noted moderation.

Outlook for FY26

India’s GDP growth has been revised upwards form the previous estimate of 7.4% for FY26, based on the old series. It is now expected to clock a 7.6% growth in FY26 against a growth of 7.1% in FY25 as per the new base year of 2022-23. In terms of nominal growth, it stands at 8.6%. The real GDP growth for FY26 looks achievable at 7.6% and is in line with our expectation. This will be on the back of remarkable double-digit growth expected in manufacturing sector (11.5% from 9.3%) which has expanded in the last 3 years. Additionally, stupendous growth is expected in trade, hospitality and tourism sector with 10.1% growth in FY26 from 6.6% in the previous year. In nominal terms, strong growth in exports (9.6% from 8.3%) along with steady growth in PFCE at 8.9% will hold ground for solid growth in FY26. This will be further supported by sharper growth in Q4 given the sustained pickup in government spending, capex, especially investment along with improved outlook for rabi sowing as well as buoyancy in consumption demand. High frequency data points (PMI-both manufacturing and services, auto sales, strong GST collections, port cargo) are already showing signs of uptick so far.

There has been reasonable traction in consumption demand amidst the recent rationalisation of GST rates. A recovery in urban consumption bodes well for the growth outlook. Notably, some uncertainty pertains on the tariff front specially US, given the recent changes. However, the new trade deals with other countries might offset any such negative impact. “Overall, we foresee limited impact of the change in the new series, with no durable bearing on fiscal ratio. With this, we continue with our forecast of 7-7.5% growth for FY27,” says the report.