While broader market holds firm, 80% of stocks slip into bear territory

Quality small caps are expected to generate superior returns hereon while large caps may remain range-bound due to high valuations and lower growth.

Surprisingly, the correction in main indices has been much lower at a 3-5% range, and even the Nifty small-cap index has fallen only ~13% from its all-time highs! (AI Image)

Indian markets have witnessed a phase of time and value correction in last 18 months (since Sep 2024) with a peculiar phenomenon where broader listed universe is in bear market territory while indices are staying near all-time/52w highs. The correction has been very sharp on the broader base of stocks in the small and midcap segment (SMIDs) of the market and the fall has accelerated in recent months, according to the latest report from Monarch AIF.

Monarch AIF cited that quality small caps are expected to generate superior returns hereon while large caps may remain in a range due to high valuations and lower growth.

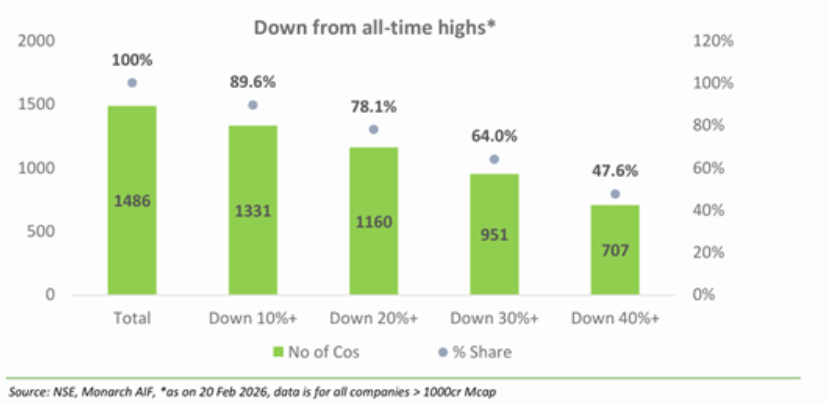

Among all listed companies > 1000cr market capitalisation (mcap), more than 64% of companies have fallen 30%+ from their all-time highs while ~78% companies have fallen 20%+ from their all-time highs. This implies that ~80% of listed universe above 1000cr mcap is in bear market category and would appear even more bleak if the companies below 1000cr mcap are included.

Surprisingly, the correction in main indices has been much lower at a 3-5% range, and even the Nifty small-cap index has fallen only ~13% from its all-time highs! This kind of divergence is very rare and within each index a narrow band of stocks have been driving the index returns in last 9-12 months while broader market remains in bear grip.

Since the broad markets have corrected sharply, the total number of quality stocks available at fair to attractive valuations has materially expanded in the last 15 months. The analysis by Monarch AIF shows that currently ~36% of all stocks above 1000cr mcap are trading at TTM P/E of below 25x (vs 25% in Sep 2024). This has made risk reward favourable for bottoms-up stock picking like it generally happens after any bear market. Monarch AIF believes that broader markets have been in bear territory for past few months and good opportunities are now emerging as several small yet fast growing companies are now available at 1Y forward P/E of less than 20x.

As per Monarch AIF, below are the factors that substantiate an entry into the broad markets, particularly small quality companies across wide range of sectors.

Smaller companies are growing faster and have consistently reduced leverage

* Earnings growth from the smaller companies (bottom half set) has been strong. CAGR for Profit before tax (PBT) stands at ~20% between 2019 and 2025; PAT growth stood at ~25%.

* The Net debt/equity for smaller companies has collapsed to 0.13x as balance sheet health remains solid

* Revenue CAGR for last three years for the companies in bottom half stood at 14% vs 11% for those in first half

Earnings growth showed improvement in Q3FY25, acceleration likely in coming quarters

* PAT growth in Q3 was impacted due to labour code provisioning. With sustenance in domestic demand and improved outlook for exports post announcements of recent trade deals with US and EU

* Monarch AIF expects the earnings growth to show further improvement in Q4FY26 and earnings upgrades could follow through in FY27E.

Lower rates provide fuel for smaller companies

As per Monarch AIF’s analysis, after every rate cut cycle involving more than 100bps, the midcap and small cap indices make a sharp recovery. SMIDs tend to benefit better from rate cuts and witness operating leverage benefits leading to better margins and bottom line growth.

Series of reforms would create multiplier effect in the long run, economic activity is improving

The Government of India has undertaken several reforms in the last 10 years but the pace and intensity of reforms have significantly increased in recent times with large income tax cuts and GST cuts executed in last 12 months which provide significant support to household balance sheets. Monarch AIF expects a strong springboard for growth for organized players across sectors and structural benefits of the reforms to flow down to the economy in coming years.