RBI Policy: No surprises as MPC holds rates, signals long pause

RBI may not have room to lower rates any further, unless the new series of CPI and GDP springs up any unforeseen surprises.

RBI’s monetary policy committee (MPC) voted unanimously to keep the policy repo rate on hold at 5.25%.

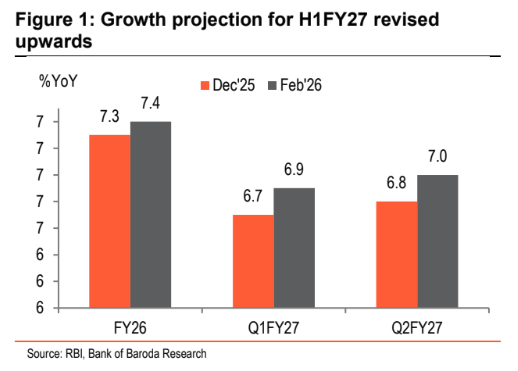

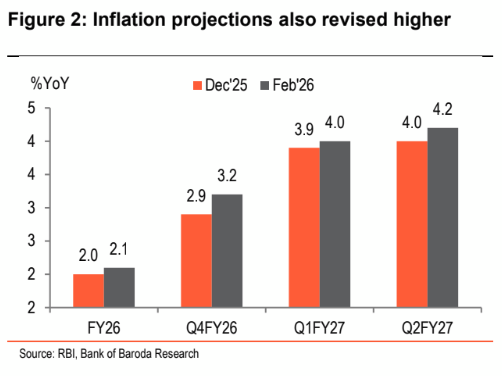

The RBI MPC in its February 6 meeting unanimously decided to keep its policy rates on hold, after lowering them by 25 bps in its last meeting in December 2025. Stance of the monetary policy was retained at neutral; Prof. Ram Singh continued to favour an accommodative stance. On the liquidity front, the RBI reiterated its support that it will maintain sufficient liquidity in the system as and when needed. Growth forecast for Q1 and Q2FY27 were revised upwards to 6.9% and 7% respectively, noting the positive impact from recently signed trade deals and continued momentum in the domestic activity. Inflation forecast for FY26 and H1FY27 were also revised higher.

“FY26 CPI is now expected at 2.1%, led by higher Q4 number (3.2%). Even Q1 and Q2 inflation is estimated to be up at 4% and 4.2% respectively. All these revisions have been made keeping in view high volatility in the prices of precious metals and unfavourable base. RBI has deferred giving its full year forecasts to Apr’26 as it awaits the release of new series this month. The Governor also highlighted that the central bank would focus on maintaining sustained growth momentum going forward. Given this backdrop and revised inflation projection, we believe that the RBI has come to an end of its rate cutting cycle and would now opt for a long pause,” said Sonal Badhan, Economist, Bank of Baroda.

MPC decision:

RBI’s monetary policy committee (MPC) voted unanimously to keep the policy repo rate on hold at 5.25%. The MPC also continued with the neutral stance, even though MPC member Prof. Ram Singh retained his view of changing the stance to accommodative.

Assessment of growth and inflation outlook:

• In line with NSO’s first advanced estimate for FY26 GDP, RBI also expects growth to come in at 7.4%. In addition, it revised its forecast upward for both Q1 and Q2FY27.

• Growth is now expected at 6.9% in Q1FY27 (6.8% in Dec’25 policy) and at 7% in Q2FY27 (6.8%).

• Upward revisions have been made noting the positive impact of two major trade deals—India-EU and India-US and continued thrust on government’s capital expenditure.

• Apart from this, rationalization of GST rates, services sector growth, higher capacity utilization, diversification of exports, and prospects of healthy rabi yield, are also expected to aid growth in the near term.

• However, downside risks may emerge from rising geopolitical tensions, uncertain global trade environment, and volatility in global financial and commodity markets.

• The MPC noted that “headline inflation during November-December remained below the tolerance band of the inflation target” and core inflation also remains benign. The upward pressure in inflation is largely due to movement in prices of precious metals, which contribute to 60-70bps.

• As a result, given the volatility in the global financial market and price of oil, in the wake of geopolitical uncertainties, and unfavorable base effect, RBI has revised its inflation projections also upwards.

• It now expects FY26 CPI at 2.1% (+10bps from Dec’25 policy), driven by higher inflation in Q4FY26 at 3.2% (+30bps). In Q1FY27 as well, CPI will rise to 4% (+10bps) and in Q2 it will increase to 4.2% (+20bps).

• Hence, inflation is expected to remain at or above the 4% level until H2FY27.

• The central bank also deferred giving the full year inflation or growth forecast as it awaits the release of new CPI and GDP series this month.

• Overall, it is expected that adequate foodgrain buffer stocks, favorable rabi sowing, prospects of good kharif sowing will keep prices in check in the near term.

Key regulatory measures:

• RBI has now permitted “commercial banks to extend finance to REITs, subject to appropriate prudential safeguards. The existing guidelines in respect of lending to InvITs are also being harmonised for parity.” This will help not only real estate firms to broaden their access to credit, but it will also help banks to diversify their investment portfolio by including more income-generating assets.

• The limit of Rs 10 lakh for collateral-free loans to MSMEs is proposed to be increased to Rs 20 lakh.

• RBI will undertake review of framework of limiting customer liability in digital transactions.

Accordingly, the draft revised instructions, including a framework for compensation in case of small value fraudulent transactions (upto Rs 25,000) will be issued.

• To protect senior citizens from digital payment frauds, the central bank will also propose measures such as lagged credits and additional authentication. It will come out with a discussion paper on the same.

• It will also issue comprehensive instructions to Regulated Entities on advertising, marketing and sales of financial products and services, to counter the problem of mis-selling financial products and services.

• RBI will undertake Review of Lending norms for UCBs. This will include:

o Raising the financial limits on unsecured loans and loans to nominal members by UCBs.

o Removal of the tenor and moratorium related requirements on housing loans given by Tier-III and Tier-IV UCBs.

o Launch of Mission-SAKSHAM (Sahakari Bank Kshamta Nirman).

• It has also been proposed that NBFCs having no public funds and customer interface, with asset size not exceeding Rs 1,000 crore, may be exempted from the requirement of registration. RBI may also dispense with the requirement for certain NBFCs to obtain prior approval to open more than 1,000 branches.

• In order to deepen the financial markets, RBI has proposed to:

o Remove the limit of Rs 2.5 lakh crore for investments under the Voluntary Retention Route (VRR).

o Issue the regulatory framework for derivatives on corporate bond indices and total return swaps on corporate bonds.

o Issue draft revised guidelines for AD banks and SPDs, allowing them more flexibility in undertaking foreign exchange transactions.

Way forward: TheRBI Governor in his statement noted that “Benign inflation provides the leeway to remain growth-supportive while preserving financial stability. We remain committed to…sustain the growth momentum”. This statement and the neutral stance indicate that the MPC has now come to an end of its rate-cutting cycle and will keep rates on hold for a long time to support growth. The Apr’26 policy will give more clarity on the outlook for full year growth and inflation. With the revision in base year, CPI is expected to inch up by 25-40bps as per our estimates. Inflation is thus expected to hover between 4-4.5%, with risks tilted to the upside. However, growth is estimated to maintain momentum and rise by 7-7.5% next year. This in turn implies that RBI may not have room to lower rates any further, unless the new series of CPI and GDP springs up any unforeseen surprises.