India’s growth story remains strong as GDP expands 7.7% in FY26

Robust growth in manufacturing, services, investment and private consumption helped India’s economy expand 7.7% in FY26, while economists expect growth to moderate to 6.4%-6.6% in FY27 amid global uncertainties, inflation concerns and monsoon-related risks.

India’s real GDP growth improved to 7.8% in Q4 FY26, after increasing by 7% in Q4 FY25. (AI Image)

India’s real GDP growth has been estimated at 7.7% in FY26, marking an improvement from a growth rate of 7.1% in FY25. On the supply side, sharp improvement was noted in manufacturing and services sectors. On the other hand, agriculture and mining output moderated. In terms of expenditure side, both personal consumption and investment growth expanded at a robust pace, underlying the growth in economic activity.

Goin ahead, headwinds to growth will require careful monitoring. External risks can have a negative impact on export and industrial output, which can also impact investments. At the same time, personal consumption could be impacted due to lower agricultural production as a result of below normal monsoon. High inflation could also come in the way of a meaningful recovery in consumption. “However, timely support from the government in the form of support to vulnerable sectors, a speedy resolution of the conflict and continued strength in the services sector will underpin growth outcomes this year. Overall, we expect GDP growth at 6.4%-6.6% in FY27,” says Aditi Gupta, Economist, Bank of Baroda.

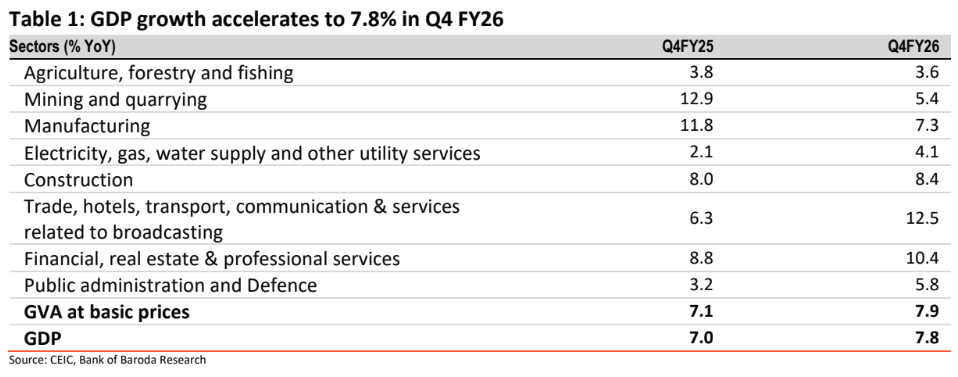

Q4FY26 GDP

India’s real GDP growth improved to 7.8% in Q4 FY26, after increasing by 7% in Q4 FY25. At current prices, GDP expanded by 9.1% in Q4 FY26 versus 9.5% growth in the same period last year. In terms of components, investment and government expenditure recorded the maximum improvement.

Growth in GFCE improved to 13.4% in Q4 FY26 versus 3.2% last year. GFCF growth also picked up to 13.2% this year, after increasing by 8.8% in Q4 FY25. On the other hand, growth in personal consumption was steady at 9.5%. The drag to growth stemmed largely from the external sector as recorded a sharp uptick. In nominal terms, exports expanded by 8.4% this year marginally higher compared with a growth of 7.9% in the same period last year. On the other hand, imports increased much sharply by 16.4% in Q4 FY25 versus 5.7% in the same period last year.

GVA growth improved to 7.9% in Q4 FY26 versus 7.1% in Q4 FY25 at constant prices. The improvement was led largely by the services sector. Service sector output increased by 9.9% in Q4 FY26 versus 6.8% in the same period last year. Significant improvement was noted in the output of trade, hotels and restaurants (12.5% in Q4 FY26 versus 6.3% in Q4 FY25) and financial, real estate sector (10.4% in Q4 FY26 versus 8.8% in Q4 FY25). On the other hand, output of mining (5.4% in Q4 FY26 versus 12.9% in Q4 FY25) and manufacturing sector (7.3% in Q4 FY26 versus 11.8% in Q4 FY25) was significantly weaker. At the same time, agriculture sector recorded almost steady growth (3.6% in Q4 FY26 versus 3.8% in Q4 FY25).

FY26 GDP

India’s real GDP growth expanded at a solid pace of 7.7% in FY26, accelerating from a growth of 7.1% in FY25. This was also higher than MoSPI’s earlier projection of 7.6% growth in FY26. Nominal GDP growth expanded by 8.9% in FY26, higher compared with a growth of 8.7% in FY25. In nominal terms, the increase was led by investment, which expanded by 9.9% compared with 8.9% in FY25. Growth in private final consumption was steady at 9.4% in FY26 versus 9.7% in FY25. Export growth also improved to 9.3% in FY26, after increasing by 8.3% in FY25. However, this was offset by an increase in imports to 11.3% (9.2% in FY25).

Real GVA growth also accelerated to 7.9% in FY26, compared with 7.3% in FY25. The rise was led largely by a solid pace of expansion in the manufacturing sector. Manufacturing output expanded by 10.7% in FY26, following up on an increase of 9.3% last year. Services output too showed improvement with a growth of 9.3% in FY26 versus 7.9% in FY25. Within services, trade, hotels, transport and communication sector recorded strong growth of 11% (6.6% in FY25). On the other hand, financial services and public admin and defence services registered steady growth. However, agriculture output moderated to 3.0% in FY26, after increasing by 4.2% in FY25.

Outlook for FY27

The growth trajectory for FY27 is likely to be impacted by a number of factors. While the West Asia crisis has not had any significant impact on India’s GDP growth last year, risks to the outlook are tilted to the downside. The continued uncertainty due to the crisis, disruptions in supply chains, elevated input costs and higher logistics costs can impact businesses and their investment decision. At the same time, exports too can get impacted. High inflation can also feed into household consumption, with rural demand carrying a greater risk. Agricultural prospects are dependent on South-West monsoon, and the high probability of below normal monsoon along with the prevalence of El-Nino conditions could impact farm output.

On the positive side, high frequency indicators for Apr’26 suggest continued resilience. Both manufacturing and services PMI indicate a steady expansion in economic activity. At the same time, bank credit growth has continued to grow in double digit. Both merchandise as well as services exports registered an impressive growth in Apr’26. Further, early results suggest that auto sales continued to register healthy growth even in May’26, led by passenger vehicles and tractors. Policy intervention by the government aimed at supporting MSMEs, exporters and other vulnerable sectors are also likely to blunt the impact of the West Asia crisis on the domestic economy to some extent. Overall, we estimate GDP growth in the range of 6.4%-6.6% in FY27.