Affordable housing financiers’ AUM to grow steady 20–21% over FY26–27: Crisil Ratings

While growth in home loans is also anticipated to be steady at ~18-20%, the loan against property (LAP) segment should see some moderation in growth.

In home loans, A-HFCs have demonstrated robust growth, outpacing the overall housing finance industry.

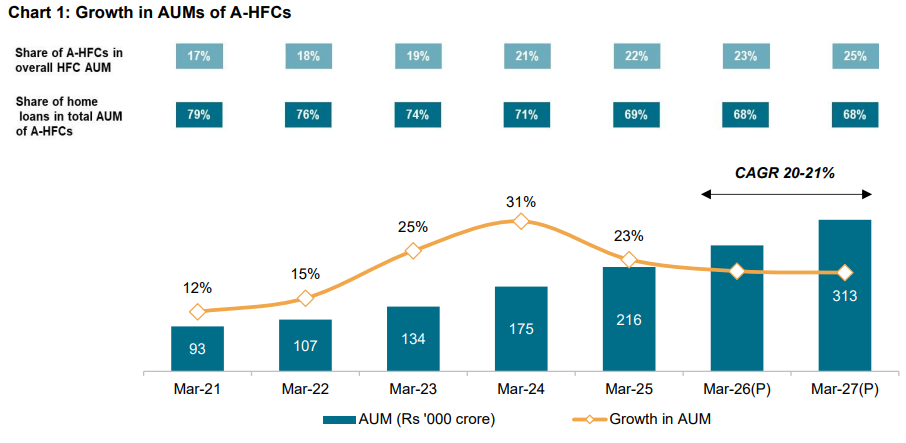

Growth in assets under management (AUM) of affordable-housing finance companies (A-HFCs) is expected to marginally moderate but stay steady at 20-21% this fiscal and next, outpacing the 18-19% growth expected for the overall mortgage finance industry. Last fiscal, their AUM had grown ~23%, according to Crisil Ratings.

While growth in home loans is also anticipated to be steady at ~18-20%, the loan against property (LAP) segment should see some moderation in growth as lenders recalibrate underwriting following asset quality pressure in some sub-categories of borrowers.

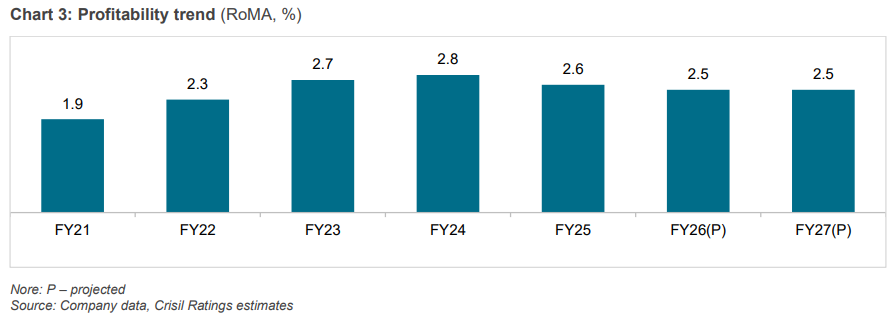

As a result, credit costs will inch up. Profitability is seen a tad lower but healthy in both fiscals.

Says Subha Sri Narayanan, Director, Crisil Ratings, “LAP, a key driver for A-HFCs in recent years due to attractive yields, will see growth moderating slightly to 24-26% this fiscal and next from ~30% last fiscal. This will be largely driven by lender prudence in response to asset quality concerns in specific sub-segments.”

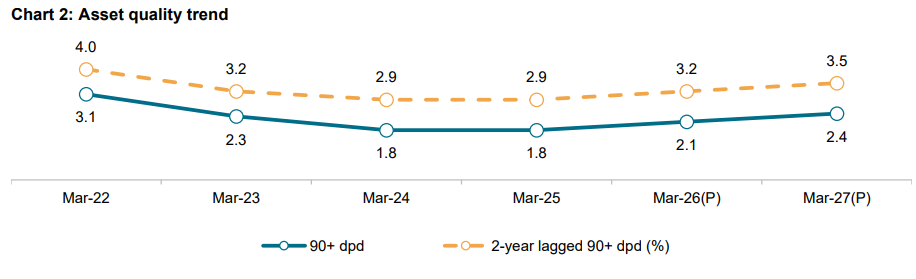

Here, the performance of small-ticket LAPs bears watching. Between fiscal 2024 and 2025, more than 70% of A-HFCs saw a notable increase in 90+ days past due loans in the sub-Rs 15 lakh category by ~25-30 basis points. The trend continued in the first half of this fiscal.

While the increase is partly due to seasoning, it is also attributable to higher borrower leverage and spillover of asset quality pressures from the adjacent microfinance customers in certain pockets. Consequently, overall asset quality metrics for A-HFCs could slip a tad but remain under control.

In home loans, A-HFCs have demonstrated robust growth, outpacing the overall housing finance industry for three reasons: relatively lower direct competition from banks compared with the prime lending segment, high growth potential fuelled by rising urbanisation, and supportive government policies for affordable-housing construction and financing. As a result, A-HFCs are expected to see a steady ~18-20% growth in home loans this fiscal and next.

However, as banks increase their presence in the prime home loan market, traditional HFCs are likely to pivot towards the affordable-housing segment, seeking to capitalise on growth opportunities and generate higher yields. The impact of rising competition on A-HFCs’ growth will therefore be monitorable.

Says Aesha Maru, Associate Director, Crisil Ratings, “From a profitability perspective, customers in this segment are less sensitive to interest rates and thus yields are expected to hold. Additionally, greater reliance on bank funding is expected to lower funding costs because bank loans reprice downwards after repo rate cuts with a lag. Furthermore, some A-HFCs offer hybrid products with an initial fixed interest rate period, which makes them less susceptible to falling rates.”

While overall credit cost is expected to increase slightly in line with delinquencies, return on managed assets is seen steady at ~2.5% for both fiscals. That would mark a modest decline of ~10 basis points from last fiscal.