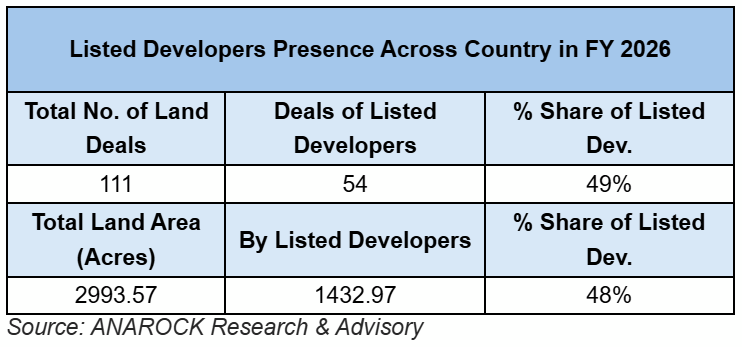

Listed developers dominate India’s land deals, account for nearly half in FY26

A total of 111 land deals covering 2,994+ acres were sealed nationwide for various real estate developments, with 54 deals over 1,433 acres executed by listed developers alone.

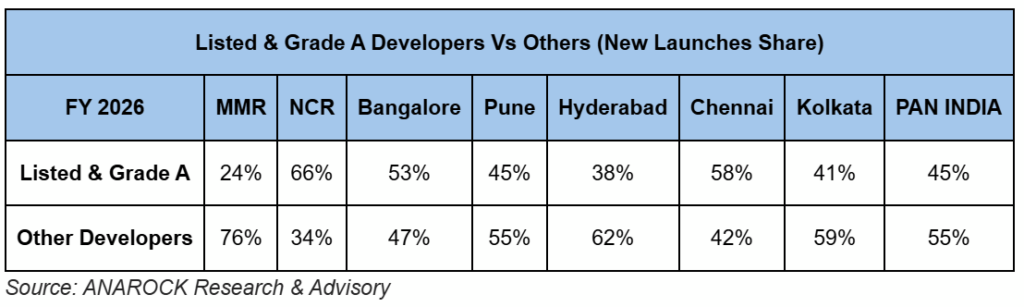

In terms of cities, NCR witnessed a notable change in its overall new supply share in the FY 2026. (AI Image)

The Indian real estate sector continues to quietly consolidate, with listed developers securing an ever-increasing and dominant share of prime land across the country. Latest ANAROCK Research data shows a moderate cooling in absolute volume of land transactions, even as its highlights the increasing hold of these dominant developers enjoy.

“Our latest data shows that listed realty players spoke for an impressive 49% share of all land deals in FY 2026,” says Anuj Puri, Chairman — ANAROCK Group. “This means that they drove close to one of every two land deals in this period. A total of 111 land deals covering 2,994+ acres were sealed nationwide for various real estate developments, with 54 deals over 1,433 acres executed by listed developers alone.”

Among the leading listed players, Godrej Properties led the pack with 17 deals across 443.5 acres, followed by Brigade Group with 8 deals over nearly 81 acres. Bengaluru emerged as the prime hotspot for listed‑player land acquisition activity in FY 2026, with around 17 deals for 293+ acres closed in the city.

- Pune saw a total of 8 land deals for approx. 78 acres closed, while MMR came a close second with 7 land deals for 51+ acres.

- Chennai and Hyderabad witnessed 5 land deals each, for 74+ acres and ~38 acres, respectively.

- NCR closed 2 land deals for 18.6 acres; Kolkata witnessed one land deal for 5 acres by listed realty players.

- Among the top tier 2 & 3 cities to attract listed players, Amritsar saw 2 land deals for a whopping 520 acres closed in FY 2026.

- Vadodara, Nagpur, Panipat, Mysore, Raipur, and Coimbatore also saw land deals concluded by listed players.

“Land acquisition is increasingly becoming both capital-intensive and regulation-driven in the last few years,” says Anuj Puri. “In this scenario, listed developers have a clear edge over unorganized or smaller players, thanks to their easier access to institutional capital and transparent balance sheets. While the total number of land deals dropped from 143 in FY2025 to 111 in FY2026, the land buying activity of these dominant players remained remarkably resilient.”

“Despite the broader market slowdown, these entities closed 54 land deals in FY 2026, nearly matching the 57 deals from the previous fiscal year. This resilience has led to a significant jump in market share. In FY2025, listed developers accounted for 40% of all land deals; in FY2026, that figure climbed to 49%.”

While these listed players’ appetite for strategic land acquisition continues unabated, it will be interesting to see how and when they will launch these projects, given the current global macroeconomic uncertainties and tapering housing sales. It is likely that they will set a more moderate tempo of calibrated new launches in the times to come.

The Sharpening Edge of Listed & Grade A Developers

An analysis of the total new housing supply (units) across the top 7 cities in FY 2026 shows that the share of the listed and Grade A developers combined stayed high at 45%. Back in FY 2025, this share was slightly lower at 43%.

In terms of cities, NCR witnessed a notable change in its overall new supply share in the FY 2026. Out of the total new unit supply in NCR in FY 2026, at least 66% was by the listed and Grade A companies. Smaller and unorganized developers comprised a 34% share.

“This clearly highlights NCR homebuyers’ rising prioritization of reliability and brand equity. NCR market has undertaken a major flight to trust, where historical delivery delays have now pushed most of the new supply into the hands of institutional giants,” says Puri.

Listed developers’ capitalizing on the surge in demand for ultra-luxury branded residences in NCR is creating a steepening entry barrier for smaller players who lack the liquidity and the ability to develop luxury developments.