Middle East ceasefire may cool chemical price rally, but supply risks linger: Ind-Ra

A temporary ceasefire may cool the recent surge in chemical prices, but supply disruptions continue to keep costs elevated.

The two-week ceasefire paves way for easing of the disrupted supply chains. However, the on-ground impact may not be fully visible till lingering uncertainties and disruption in the Strait of Hormuz persists. (AI Image)

India Ratings and Research (Ind-Ra) opines that the Middle East ceasefire could ease supply‑shock fears and the resultant rally in chemical costs, but the lingering uncertainties would keep prices across crude oil and natural gas derivative chains elevated until supply chains normalise.

“Prices are likely to remain higher than pre-conflict levels in the near term, given the logistics and supply disruptions. Continued conflict may increase volatility, potentially affecting sector recovery,” says Khushbu Lakhotia, Director, Corporate Ratings, Ind-Ra.

Most of Ind-Ra’s rated large chemical issuers remain investment-grade, supported by diversified end-markets, prudent financial policies and adequate liquidity. However, rating headroom has narrowed for a portion of the portfolio amid prolonged weak pricing before the beginning of the conflict, uneven demand recovery and delays in deleveraging, following recent capex cycles. While liquidity buffers are adequate for most A-category and above issuers, stress could build for leveraged and capex-heavy companies, leading to certain segments of the sector facing sustained downside risks. Around one-fourth of large rated chemical exposures carry a negative outlook, reflecting heightened sensitivity to margin and cash-flow volatility.

Supply-Chain Risks Persist until Sustained De-escalation

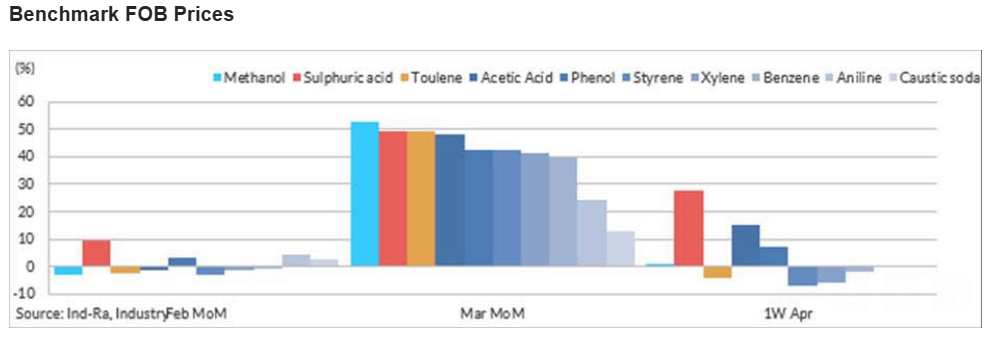

Ind‑Ra opines that the two-week ceasefire paves way for easing of the disrupted supply chains. However, the on-ground impact may not be fully visible till lingering uncertainties and disruption in the Strait of Hormuz persists. The conflict has materially impaired global chemical supply chains, given the region’s importance in base chemicals such as methanol, ammonia, polyolefins and styrenics.

The methanol value chain is among the most vulnerable, with the Middle East accounting for nearly a third of global exports and Iran being a major producer. Disruption cascades into downstream segments, including acetic acid, vinyl acetate monomer (VAM), formaldehyde and methyl tert-butyl ether (MTBE), affecting end-use industries such as construction, paints, adhesives and automobiles.

India imports an estimated 15%–20% of its chemical requirements from the Middle East. Value chains with high dependence on the Middle East sourcing or gas-based feedstocks could face utilisation pressure in 1QFY27, as inventories deplete faster than supply chains normalise—amid ongoing logistics constraints and the gradual restoration of capacities affected by force majeure or damage. Companies with diversified sourcing and access to integrated suppliers are better positioned to mitigate these risks. While supply disruptions also affect China’s derivative production, the impact could be partly offset by its lower import dependence and coal-based chemical capacity.

Customs Duty Waiver to Offer Limited, Near-Term Relief

Ind-Ra believes the government’s announcement of a three-month customs duty exemption on about 40 chemicals would provide moderate, short-term relief, with landed costs likely to decline by 5%–10% (depending on the product and prior duty structure), bringing some relief to chemical companies dependent on these feedstocks and relevant downstream industries, such as like plastics, auto, and paints. Domestic producers of these chemicals will see a reduction in the import-parity price.

Recent price increases of 30%–50% across several chemicals could result in short-term inventory gains, given the typical holding periods of one-to-three months. Beyond this, margin outcomes will depend on cost pass-through capability, inventory and forex management, and supply-chain execution. However, a sustained de-escalation of the conflict could lead to some price correction, reversing inventory gains. The sector witnessed revenue growth in 3QFY26 despite the high US tariffs, while maintaining range-bound EBITDA margins.

Uncertainty Driving Discretionary Deferrals, Underlying Demand Impact to remain Contained

Ind‑Ra expects the crisis to have limited impact on demand. While exports to the Middle East are likely to remain affected until tensions ease, the region accounts for only a high single-digit share of India’s chemical exports. Shipments to other markets have largely remained resilient despite longer transit times and higher logistics costs.

The recent reduction in US tariffs could support export growth, with the US accounting for about 15% of India’s chemical exports, while Europe may offer incremental opportunities amid rising local production costs. Domestically, demand remains supported by agriculture- and pharma-linked consumption, which together account for around one-third of total chemical usage. Essential and contract-based segments are likely to remain relatively stable, though discretionary buying could be deferred as uncertainty and a likely price correction with the ceasefire would limit channel offtake to immediate requirements.

Prices seen Higher than Pre-conflict Levels; Margin Outlook Mixed

Supply disruptions have led to a sharp increase in prices, with methanol and several aromatics rising 30%–50% on a mom basis in March 2026, triggering inflation across downstream value chains. Ind-Ra believes many players could register inventory gains during March-April 2026, but products spreads could be affected in segments with inadequate price pass-through. Despite typically higher pricing power, price transmission in specialty chemicals is largely determined by bilateral contract negotiations and inventory levels. While prices could correct once geopolitical tensions ease—particularly in segments facing structural oversupply—Ind‑Ra expects them to remain above pre-conflict levels in the near term, given the impact on supplies for some of the starting inputs and building blocks.

Profitability impact is likely to vary across the sector. Some players may benefit from inventory and forex gains, while import-intensive commodity manufacturers could face margin pressure. The near-term EBITDA margins likely to be impacted by an interplay of the following factors: i) the ability of players to pass on cost inflation; ii) inventory and forex management strategy; and iii) supply chain management. Companies with FOB sale contracts are relatively better placed, while others are trying to re-negotiate contracts to pass on freight costs on cost, insurance and freight contracts.

The EBITDA margins remained flattish yoy at around 13% in 3QFY26 (2QFY26: 14%; 3QFY25: 13%), below the median of around 15% over the cycle. However, despite weak pricing and the impact of US tariffs, the sector recorded a revenue growth of about 7% yoy in 3QFY26, supported mainly by volume recovery in specialty and agrochemicals.

Liquidity Adequate, Though Stress Pockets Persist

Working capital requirements have risen in many segments due to higher input costs and elongated supply cycles, though the impact of the same is partially offset by increased payables. Capex activity remains cautious, with a focus on committed and maintenance projects. While liquidity buffers are adequate for most A-category and above issuers, stress remains elevated for leveraged and capex-heavy companies, resulting in certain segments facing continued downside risks.

India Ratings and Research (Ind-Ra) has published the April 2026 edition of its Chemicals Insights report, covering segmental performance trends for the sector.