FY26 Bond Wrap: Why India’s 10Y yield refuses to ease

After a soft start, India’s 10Y yield turned sticky in H2FY26 amid rising supply concerns and global geopolitical tensions. Oil shocks and volatile capital flows have added to upside risks, keeping yields elevated.

India’s 10Y yield has exhibited considerable degree of stickiness towards the latter part of FY26. (AI Image)

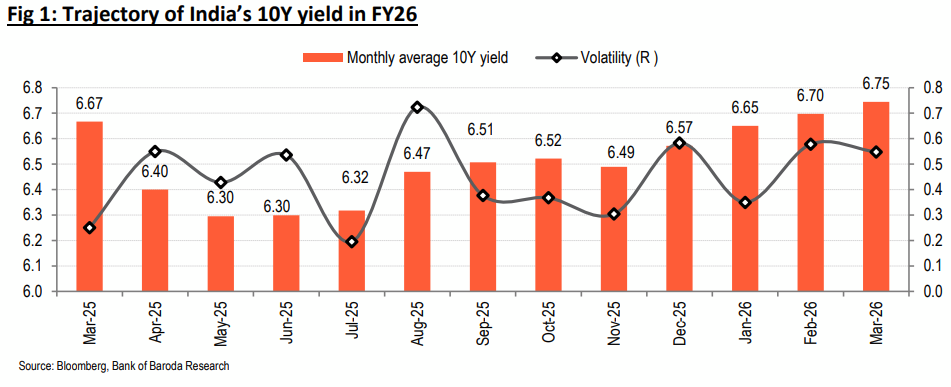

India’s 10Y yield witnessed considerable volatility in FY26. The first half showed a softening bias supported by favourable inflation, easing monetary policy cycle and liquidity measures by the RBI.

However, towards the H2 of FY27, it has exhibited considerable stickiness. This was on account of concerns about the excess supply of securities. Now, with the ongoing West Asia crisis in place, the reverberation on India’s yield has been significant as India is a major oil dependent economy. Thus, fiscal and inflationary concerns could not take a backseat albeit from the standpoint of a much comfortable macro fundamentals, yet in place, according to a Bank of Baroda research report.

“We expect the stickiness in India’s 10Y yield to persist for now, unless the war situation de-escalates,” it says.

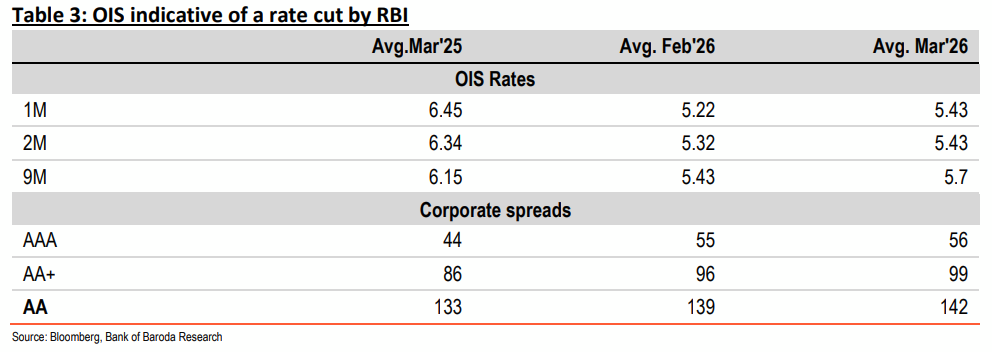

The OIS rates are also indicative of a rate hike in the near term. For Apr’26, we do not expect any rate action by RBI as data dependent approach may be the preferred choice in a volatile global financial landscape. We expect India’s 10Y yield to trade in the range of 6.9-7.10% in the near term, with an upward bias.

How India’s 10Y yield have moved in FY26:

The trajectory of India’s 10Y yield in FY26 has been interesting. The initial months got support from faster pace of frontloading of rate cut by RBI along with liquidity infusion measures. However, since Dec’25 onwards, India’s 10Y yield saw an increase. The volatility exacerbated amidst ongoing geopolitical conflict and its reverberations were felt across major asset classes. So, what has led India’s yield to be sticky with an upside bias?

The factors which impacted its movement in FY26 are illustrated below:

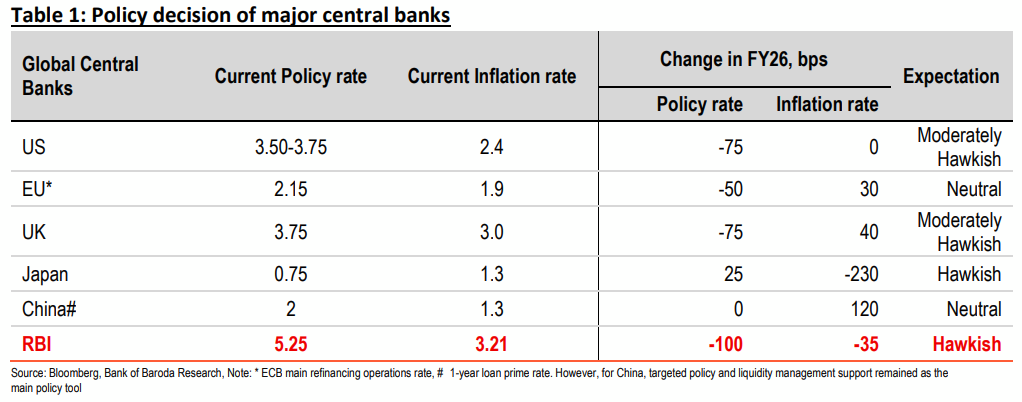

1. Global central banks and India: Broadly global monetary policy has been accommodative in FY26 for major central banks as inflation broadly remained within targeted level, albeit tariffrelated uncertainty. For Fed, major officials in their statement reiterated risks from higher energy prices. One of the officials (Chicago Fed President) explicitly spoke about rate hike. The SOFR rate (US secured overnight financing rate) is hovering at 3.63%, signaling no rate action from Fed. The future course of Fed fund rate is contingent on a concomitant of economic and political factors.

The Table 1. shows future policy action is migrating between neutral to moderately hawkish based on the underlying growth-inflation dynamics and depending on the length of the war.

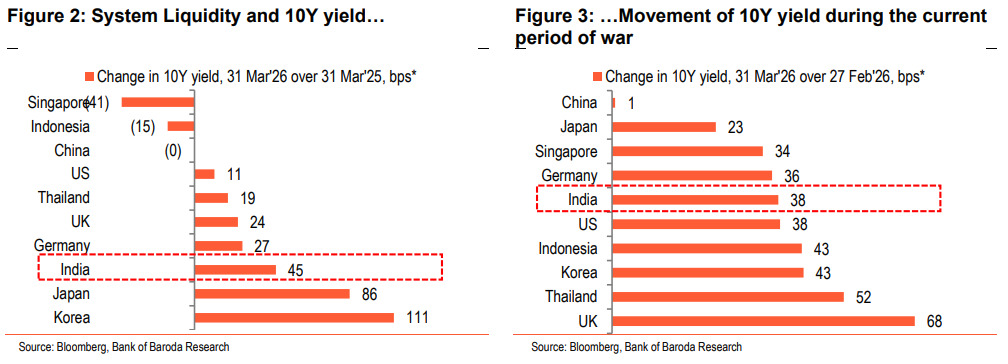

A) Convergence or divergence with global yields: India’s 10Y yield witnessed considerable spike in FY26. It rose by 45bps, next to 111bps increase in 10Y yield of S. Korea and 86bps increase in 10Y yield of Japan. For Japan, increase in policy rate from a long standing ultra-low rate contributed to the same. For India and S. Korea, the major jump happened during the war period as both economies are dependent on energy imports.

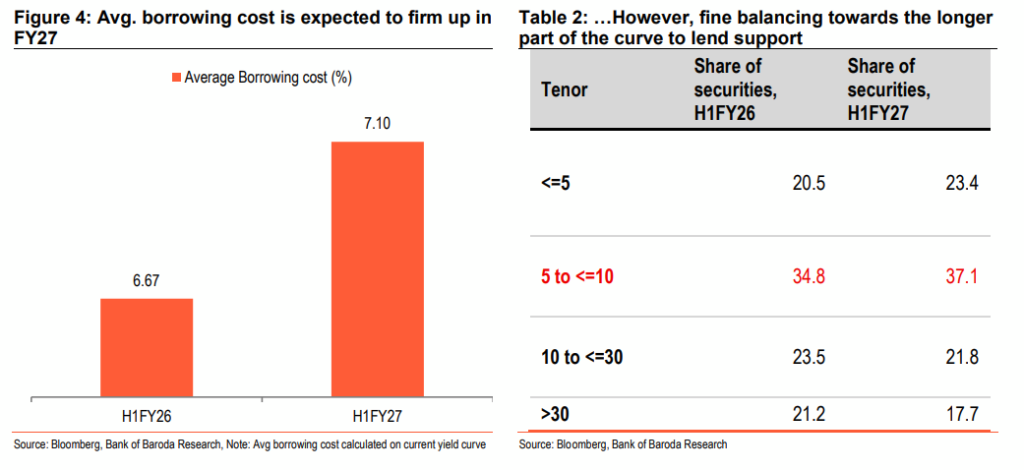

2. H1FY27 Borrowing is finely balanced: H1FY27 centre’s borrowing is pegged at Rs 8.2 lakh crore. However fine balancing of securities with lesser pressure towards ultra-long portion of the curve (>30-years) is expected to put less pressure on the longer end of India’s yield curve.

The average borrowing cost is expected to inch up to 7.10% in H1FY27.

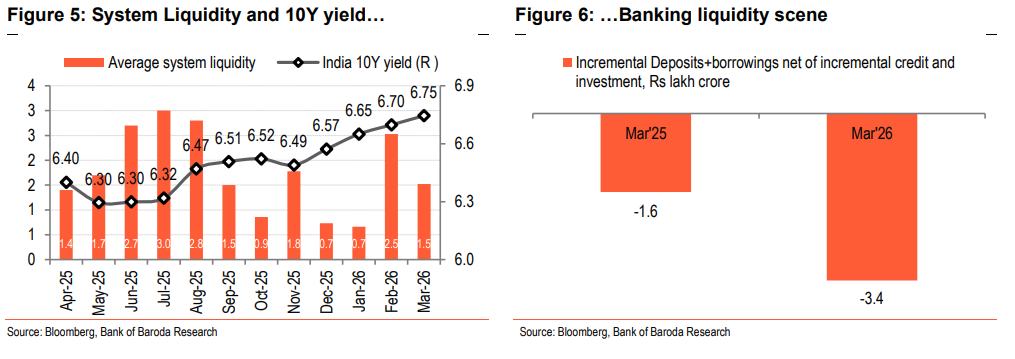

3. Movement of India’s 10Y yield and domestic liquidity: There has been significant correlation between movement of system liquidity and India’s 10Y yield. Domestic liquidity strain was visible in H2 of FY26. However, RBI’s support through LAF and durable liquidity infusion measures (OMO, swap) provided the necessary cap to yields. This year witnessed highest OMO purchase by RBI to support durable liquidity (Rs 8.8 lakh crore, Source: Bloomberg data on RBI purchase of GSec in secondary market).

The banking liquidity scene also mirrored system liquidity. Higher credit demand led to increased gap between incremental deposits and borrowing net of incremental credit and investment. There is no reigning pressure on durable liquidity (running at ~ Rs 5 lakh crore) which was supported by RBI’s measure. However, if the depreciating pressure on INR reigns and credit growth is buoyant, the pressure on liquidity would mount. Currently, the level of system liquidity, is at 0.9% of NDTL (NDTL as of 15 Mar 2026).

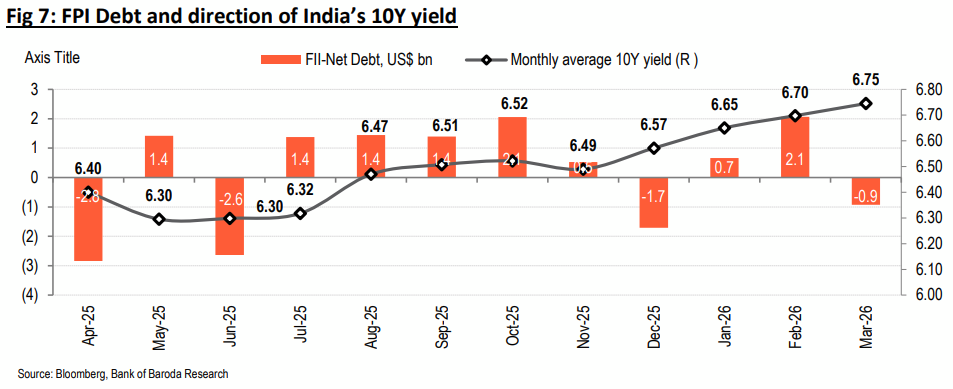

4. Movement of India’s 10Y yield and FPI-Debt flows: FPI debt flows remained volatile throughout FY26. The stickiness in India’s 10Y yield coincided with net debt outflow. The current outflow also coincides with volatility in global political landscape. Thus, unless geopolitical conflict gets corrected, volatility in debt flows is likely to persist and would put pressure on yields.

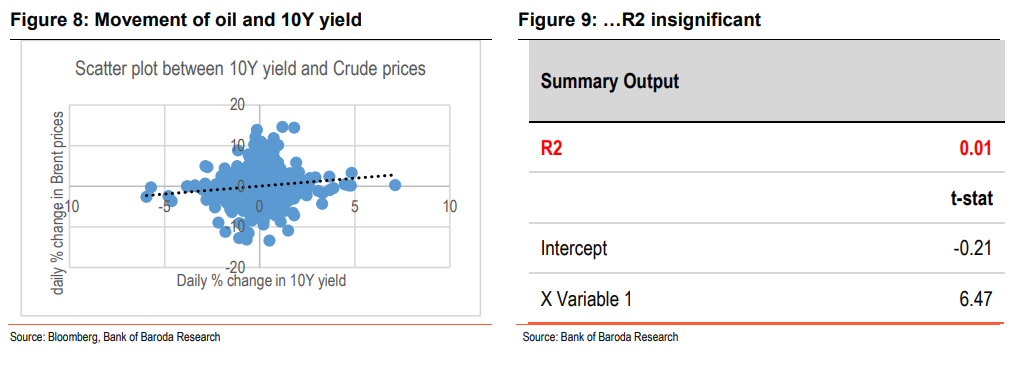

5. India 10Y yield and oil: The upswing in 10Y yield coinciding with the geopolitical crisis generally put forward the question of linkage with global oil prices. However, historically, there has been no significant correlation between the two. The channel of impact on 10Y yield is mostly through inflation rather than directly oil prices impacting yield.

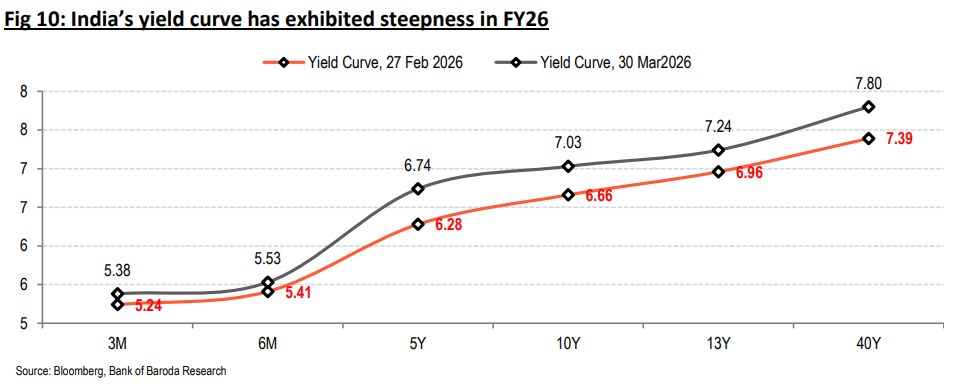

Fig 10. shows long-end part of the curve witnessed significant upward correction in the last one month. The gap between short and long end part of the curve increased to 242bps, as on 30 Mar’26 from 215bps, as on 27 Feb 2026. It is worth mentioning that as on 28 Mar 2025, the gap was much lower at 61bps. Thus, considerable steepness in India’s yield curve was seen in FY26. Finely managed government borrowing program might lend some support. However, for now we expect similar trend in steepness of India’s yield curve to continue.

Other market rates: OIS inched up signaling some anticipated rate action by RBI. However, corporate bond spreads remained broadly on similar levels even during the period of war.

Outlook on 10Y yield:

India’s 10Y yield has exhibited considerable degree of stickiness towards the latter part of FY26. In fact, the steepness in India’s yield curve is significant when compared to Mar’25. The ongoing geopolitical crisis has put more pressure on yields as fiscal and inflationary concerns couldn’t be avoided due to India’s major reliance on energy import. However, we are starting off on a much more comfortable space where inflation is already below RBI’s targeted level.

Growth is on a stable footing. Thus, against this backdrop, we feel RBI would be in a wait and watch mode and any future action will be data dependent. We do not expect any change in rate or stance in the upcoming policy. However, policy undertone may be hawkish with inflationary concerns back in picture. We expect yields to remain in the range of 6.9-7.10% in the near term, with risks tilted to the upside. However, any signs of resolution of the West Asia crisis will likely result in correction of India’s 10Y yield since the other factors (such as liquidity, prudent management of government borrowing across the yield curve) are supportive of a moderation in yield.