Budget 2026 incentives set to accelerate municipal bond issuances: Ind-Ra

Ind-Ra believes larger size single bond issuances would materialise gradually; however, the medium-term outlook for municipal bond activity remains strong.

The budget introduces a new incentive of INR1,000 million for every single municipal bond issuance exceeding INR10,000 million. (Image: AI Generated)

India Ratings and Research (Ind-Ra) opines that the Union Budget 2026-27 will strengthen supply-side dynamics in India’s municipal bond market. The enhanced financial incentive structure is expected to accelerate market participation, encourage greater reliance on debt capital markets for urban infrastructure funding, and promote financial and operational discipline in municipal corporations, says Anuradha Basumatari, Director, Public Finance, Ind-Ra. Ind-Ra believes larger size single bond issuances would materialise gradually; however, the medium-term outlook for municipal bond activity remains strong.

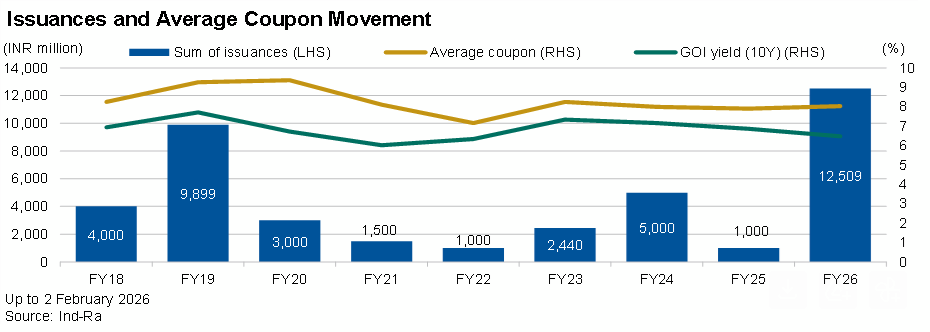

Urban local bodies’ (ULBs) obligatory function is to provide access and quality essential services to its citizens. However, financing constraints have historically hindered infrastructure creation and service quality. Since the introduction of municipal bond guidelines in 2015 and the launch of Atal Mission for Rejuvenation and Urban Transformation (AMRUT) incentives in October 2021, ULBs have increasingly explored bond issuances, although volumes remain modest. A supportive regulatory framework along with central government incentives under AMRUT has already enabled several ULBs to access bond markets since 2017. As of 2 February 2026, there have been 28 municipal bond issuances by 21 ULBs in the market aggregating INR40,347.50 million since FY18 (outstanding: INR35,847.35 million). The largest single issuance of INR2,440 million was by Indore Municipal Corporation in FY23. Bond issuances were steady during 10MFY26, aggregating INR12,508.50 million, exceeding the earlier highest annual issuance of INR9,899 million reported in FY19. Ind-Ra expects further issuances in the near term, with ULBs such as the Nashik Municipal Corporation (green bond) actively working toward their bond issuances.

The budget introduces a new incentive of INR1,000 million for every single municipal bond issuance exceeding INR10,000 million. Ind-Ra expects that it will encourage large ULBs to access debt capital markets to fund large-scale urban infrastructure developmental works while strengthening their financial discipline and governance. Existing incentive provisions under the AMRUT framework will continue, ensuring support for small and mid-sized ULBs. Earlier provisions were as under:

A first municipal bond issue qualifies for an incentive equal to 13% of the amount raised, i.e., INR130 million for every INR1,000 million raised, up to a maximum of INR260 million.

For any second or later bond issue, ULB must issue it as a green bond – limited to sectors such as water, sanitation, renewable energy, or urban resilience. Such issues are eligible for INR100 million per INR1,000 million raised, with the incentive amount capped at INR200 million.

There are limited green issuances in the market. Some of them include Ghaziabad Nagar Nigam, Indore Municipal Corporation, Ahmedabad Municipal Corporation, Vadodara Municipal Corporation, Surat Municipal Corporation, and Pimpri Chinchwad Municipal Corporation.

The 16th Finance Commission (FC) has recommended INR2.32 trillion as basic grants for ULBs and INR290.16 billion based on performance of ULBs for the award period FY27-FY31. The 16 FC has also recommended a special infrastructure component grant of INR561 billion (FY27-FY31) for select cities with a population of between 1 million to 4 million (as per Census of India 2011), which is tied to the development of wastewater management projects. These would be large-scale projects, to be funded in the ratio 60:40, with the union government funding 60% of the project cost and 40% contribution by the state government and concerned ULB. The financial incentive framework and the special infrastructure grants support targeted at large cities have created a favourable environment for financially strong ULBs to fund capex through a mix of own funds, grants, and market borrowings.

ULBs are still testing the waters with issuance sizes largely limited to INR2,000 million. The coupon rates for municipal bond issuances during FY18–10MFY26 was in the range of 7.15%-10.23%. The average spread of municipal bonds over the 10-year government of India (GoI) yield was 142bp during FY18 to 10MFY26. Bond pricing continues to be influenced by several factors, including the prevailing interest rate environment, bond tenure, credit rating, inflation expectations, and liquidity of the bond.

The enhanced financial incentive, alongside existing provisions, holds considerable promise for municipal bond activity by encouraging ULBs to undertake both new and repeat issuances. With stable inter-governmental fiscal transfers, a supportive regulatory environment, and continued AMRUT incentives, Ind-Ra expects greater debt market participation by ULBs of varying sizes in the medium term.

Ind-Ra expects large-scale issuances will materialise gradually in due course of time, as ULBs need time to: (a) identify viable projects, (b) obtain requisite approvals, and (c) develop sustainable funding structures. Large ULBs, which have historically relied predominantly on bank loans and have only partially tapped the bond market, may now be more inclined to utilise bond issuances to take advantage of the enhanced incentive framework.