FY-end boost lifts credit card spends, but growth slows to 9% in March: CareEdge Ratings

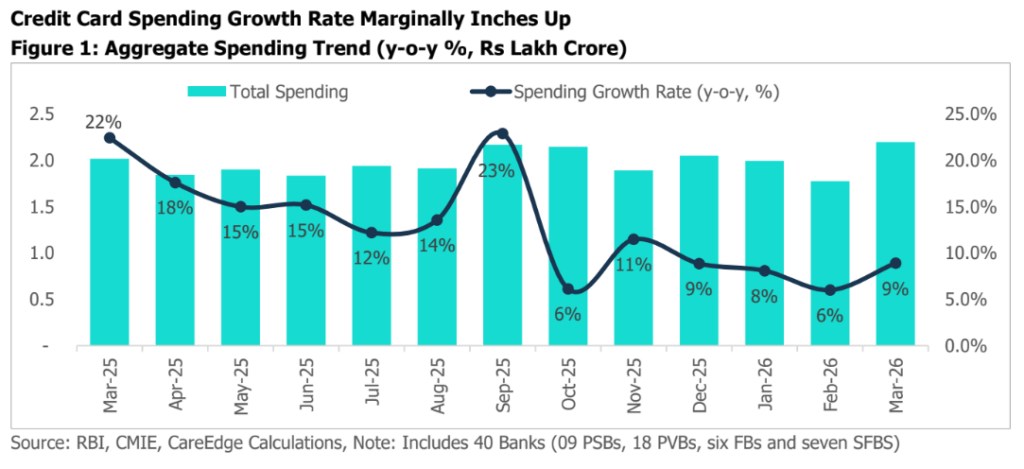

March 2026 saw a marginal recovery in credit card spending on a sequential basis. However, y-o-y growth remained subdued at 9.0% versus 22.4% in March 2025, primarily due to the base effect.

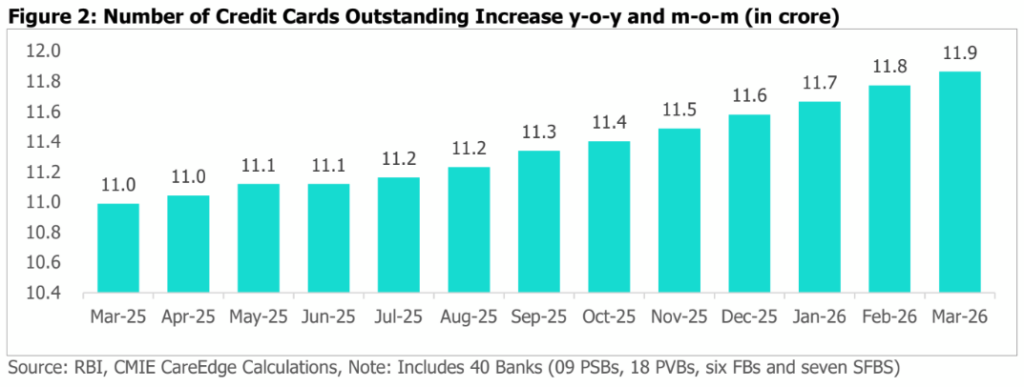

The overall credit card base increased to 11.9 crore as of March 2026, growing 8.0% y-o-y and 0.8% m-o-m. (AI Image)

In March 2026, credit card spending rose by 9.0% y-o-y to Rs 2.20 lakh crore due to sustained e-commerce spending. This was marginally higher than 8.9% growth seen in February 2026 on account of seasonality in the month with spending picking-up typically towards fiscal-year-end. In comparison with growth of 22.0% in March 2025, monthly growth moderates y-o-y due to the base effect, according to CareEdge Ratings.

The overall credit card base increased to 11.9 crore as of March 2026, growing 8.0% y-o-y and 0.8% m-o-m. “Growth in outstanding cards continued to be led by PSBs, which grew by a healthy 11.3% y-o-y on the back of their wider distribution network and gaining traction through co-branding partnerships with e-commerce merchants and fintechs. SBI Group continues to be the key growth driver within PSBs, with outstanding cards increasing by 6.1% y-o-y to 2.21 crore cards as of March 2026,” it says.

• Private sector banks (PVBs) posted a healthy growth of 8.3% y-o-y in their card base. However, this was lower than 9.1% seen in February 2026, indicating selective growth in certain players rather than broad-based across the sector. This reflects these banks’ continued scaling of their retail franchise, aided by improved execution.

• Foreign banks continued to pare down their card portfolio with outstanding cards declining 5.4% y-o-y, continuing the trend of last few quarters. This decline is partly attributable to portfolio rundowns as well as structural shifts (such as portfolio sales), leading to foreign banks’ card base getting redistributed to domestic banks.

Key takeaways

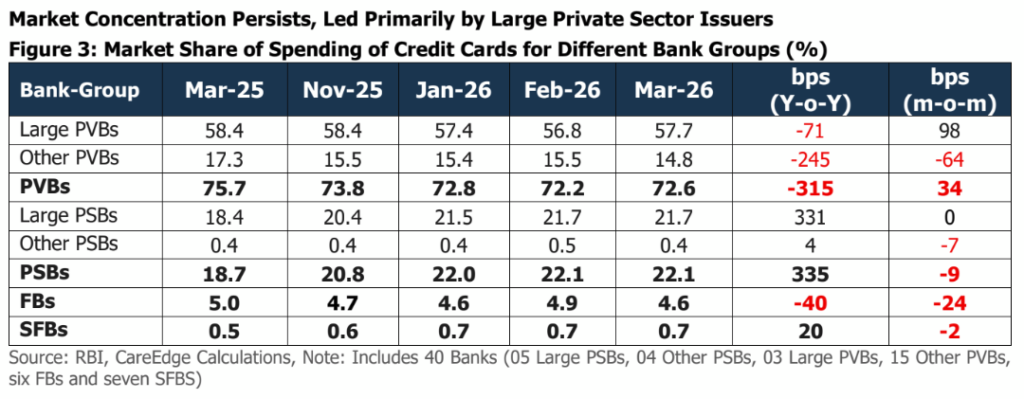

* Credit card spends moderated by around 85 basis points (bps) y-o-y but remained robust m-o-m aided by typical seasonality. Despite moderation in credit card growth seen over the last couple of months, the credit card market continues to remain highly concentrated with the top five issuers accounting for more than 80% of the spends.

* Market share of PVBs dropped by 315 bps y-o-y, largely due to the contraction of the base of small- and mid-sized PVBs while market share of large PVBs remained largely stable. The decline in market share of other PVBs in March 2026 continues to reflect their selectiveness towards card issuance as well as credit limit upgrades, pointing towards tighter underwriting standards and lower risk appetite.

* PSBs continued to gain share in credit card spends. Market share of PSBs improved by 335 bps y-o-y to 26.7% in March 2026 led by the growth in card base of large PSBs. Growth in PSBs’ share is driven by their increasing penetration in nonmetro markets (tier-2 and tier-3) as well as growing use of credit cards linked to UPI. On a sequential basis, PSBs’ share. However, PSBs continue to account for a relatively smaller share of the total card spends at 22.1%, given its contribution is skewed towards a few large players. Share of other PSBs improved marginally y-o-y from 0.4% to 0.5% reflecting continued broad-based basing. On the other hand, PVBs continue to command a larger share in high-value spends driven by their continued dominance in premium cards and higher share of fee-income generating customer profiles.

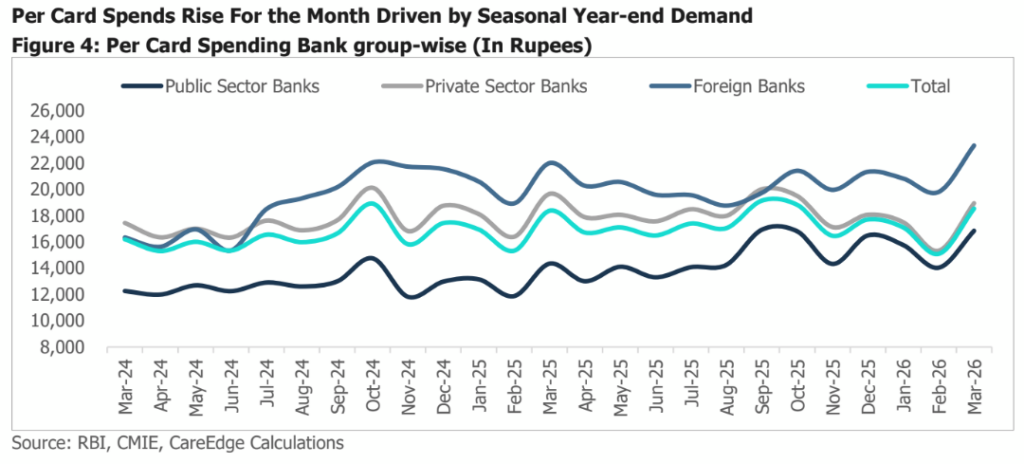

* Monthly per-card spends picked up sequentially in March 2026, growing by 23.0% m-o-m to Rs 18,536, as compared to the decline of 14.0% seen in February 2026 led by fiscal year-end spending. Additionally, growth in traction towards UPI linked credit cards for small ticket spends is also contributing towards higher spends. However, when compared to March 2025, per card spends grew by a mere 1.0%, indicating base normalisation.

* At the bank-group level too, the difference in average spends between PVBs and PSBs continued to narrow further. Average spends per card for PVBs declined by 4.0% y-o-y to Rs 18,948 driven by dilution in spends as card issuances continue to pick-up across mass and new-to-credit customers who traditionally display lower utilisation in initial years. PSBs, on the other hand, continue to trend towards their typical double-digit growth path, recording a healthy 17.0% y-o-y growth in average spends per card to Rs 16,847. This is supported by better customer engagement as well as greater adoption of credit cards linked to UPI. With the growth of UPI linked credit cards, we are starting to see a structural shift in credit card spends where issuers who are quick to integrate their cards with UPI start to see some of the incremental transaction volumes flowing through their systems.

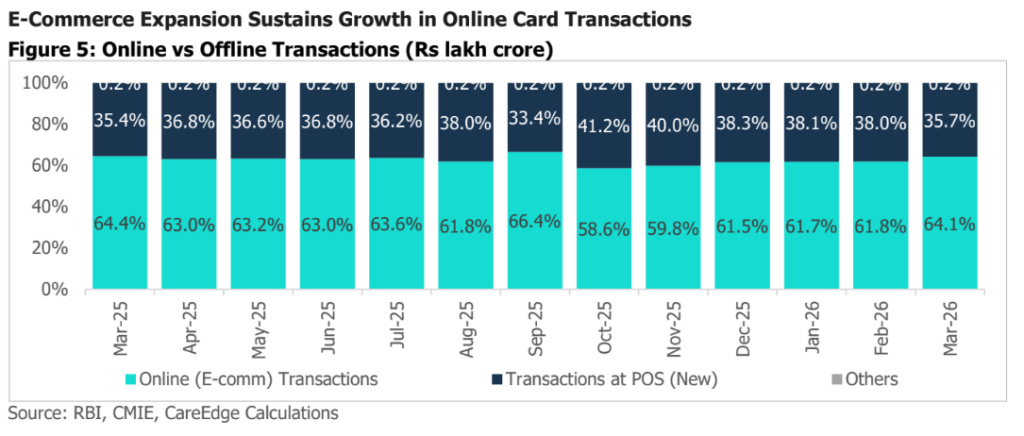

* Digital continued to dominate credit card spends with a share of over 61% in March 2026, in line with what we have observed throughout FY26. Credit card spends towards ecommerce transactions grew by 8.4% y-o-y during the month.

* Point-of-sale (POS) transactions also saw higher growth of 9.8% y-o-y compared to growth in digital spends, reflecting recovery in spends towards offline transactions. Incremental spends continue to be skewed towards digital transactions.

• PSBs continued to lead growth in both online and offline spends across categories. E-commerce transactions for PSBs grew by 39.1% y-o-y led by accelerated digital adoption and engagement.

* POS transactions for PSBs grew by 11.1% y-o-y reflecting improvement in ground level acceptance of credit cards.

Conclusion

Overall credit card spends in FY26 grew by 12.0% y-o-y to Rs 23.6 lakh crore, building upon the strong resilience in card led consumption seen during the previous year. Credit card spends grew 14.0% y-o-y in FY25. Growth in spends during March 2026 was aided by seasonality as spends typically pick up towards year-end. Y-o-y growth moderated due to high base in the year-ago period.

The slowdown in growth of spends in FY26 versus FY25 is due to base normalisation after strong demand post pandemic, dilution in spends per card with accelerated card issuance in recent years (especially mass and new-to-credit customers who typically have lower utilisation in the initial years) and a gradual shift of low-value spends towards UPI linked credit instruments.

Credit card spending growth is expected to remain stable and moderate going forward despite near-term headwinds such as cyclical normalisation in discretionary demand and base effects. Structural tailwinds such as continued addition to the card base (which is now being driven by PSBs), gradual uptick in usage of credit cards linked to UPI and improving credit card utilisation are expected to drive credit card spending growth in the coming years as the benefits of new portfolio seasons play out.

However, private sector banks are adopting a more calibrated approach, with increased focus on profitability reflected in the rationalisation of rewards programmes, tighter underwriting, and selective customer acquisition, which may keep their growth measured.