March CPI inflation rises to 3.40% as fuel, housing push prices up

CPI inflation inched up to 3.40% in March, driven by rising imported costs and pressure from fuel and housing segments.

All-India core inflation only decreased by 2 bps to 3.38% in March 2026, with the state-wise trend being quite divergent. (AI Image)

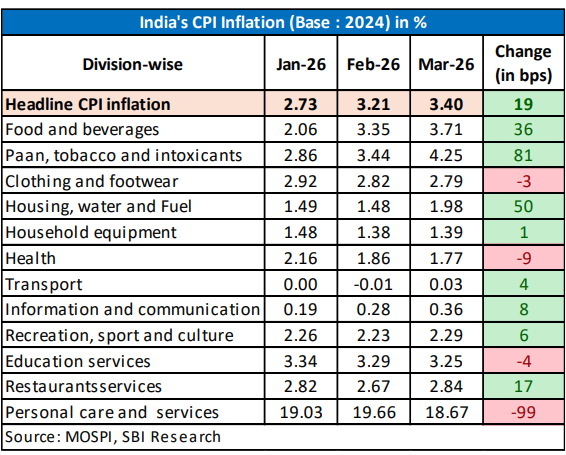

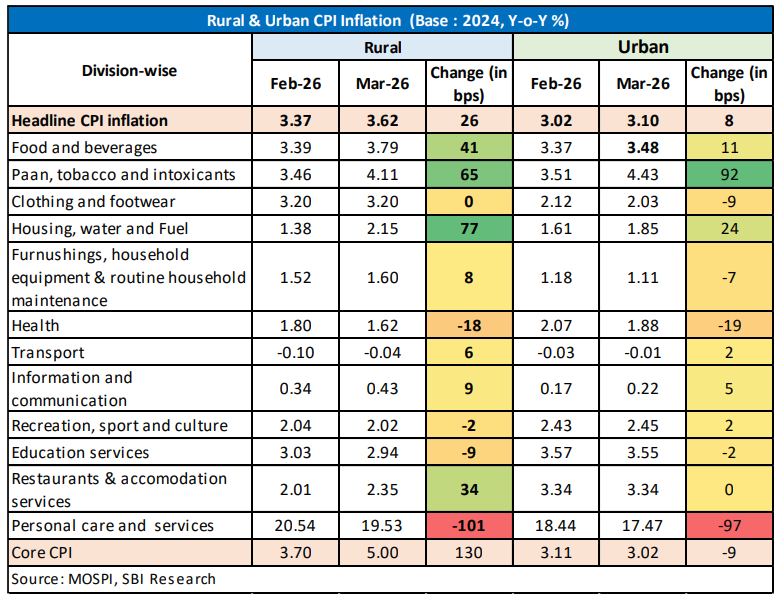

Consumer Price Index (CPI) inflation rose to 3.40% in March 2026, third time consecutively, up from 3.21% in February 2026, driven by rising prices of two divisions (paan, tobacco and intoxicants as also housing, water and fuel). Personal care and services exhibited significant decline due to moderation in gold and silver prices. All-India core inflation only decreased by 2 bps to 3.38% in March 2026, with the state-wise trend being quite divergent. Overall, the state-wise trend is mixed, in some states the core is greater than overall and in others core is less, according to SBI Ecowrap.

Owing to exchange rate fluctuations and external shocks like supply chain disruptions, the imported inflation (weight: 21.84%) rose to 6.49% in Mar’26 as compared to 6.35% in Feb’26. The weighted contribution of imported inflation in overall inflation is now 43%. Rural and Urban CPI inflation both increased in Mar’26 compared to Feb’26, indicating a mild upward movement in price levels across both segments.

Meanwhile, IMD has predicted a deficient rainfall during the current fiscal with southwest monsoon at 92% of the LPA (slightly worse than SkyMet’S projection of 94% last week) that has stoked fears of disruption on already fragile agri output front. Basis our study, years with relatively comfortable rainfall have still witnessed elevated food inflation such as 98% rainfall with 8.43% food inflation in FY09, 102% with 15.2% in FY11 while weaker rainfall years such as 93% (FY13) and 91% (FY19) were associated with much lower food inflation of 6.33% and 0.09%, respectively.

Also, the buffer situation of the foodgrains (more so on rice front at 380 LMT) looks sufficient to thwart any untoward disruption on Kharif production front, if it be so. As a solace, food production too has apparently little co-relation with rainfall pattern, even the years with lower than LPA rains witnessing good output. What is important is the spatial distribution.

Separately, the outflows led by FPIs have been unabated post the Central Bank measures in last few days, ~$6.9 bn in total while rupee may lose its regained strength as volatility increases in global markets in lockstep with heightened hostility across West Asia, signifying it’s the structural reforms anchoring BoP that would have a sobering effect on the rupee’s slide, and not just some immediate solutions that in turn pose challenge to genuine investors and financial intermediaries quest for suitable hedging mechanisms as India seeks higher capital flows.

Meanwhile the tacit move of US seems to be multi fold, we believe; forcing Asian majors (to pressurize Tehran to come to deal table), nudging NATO to reconsider its approach should the aggression reach another territory and enabling select oil behemoths to have a larger say in the alternate supply chains that may continue even when conflict is amicably resolved.