Rupee Under Strain: Time for clear, unambiguous policy support

Despite strong macro fundamentals and ample forex reserves, rising volatility and structural pressures call for calibrated RBI intervention to stabilise the rupee.

There is still time to intervene in the market to prop up the rupee if it is so desirable. (AI Image)

Unprecedented times call for unequivocal, unprecedented and unambiguous supports. With parallels rife between 2013 and present in terms of supporting the rupee, it is pertinent to understand the differences between the two periods, one checkmated with umpteen doubts on the fiscal health of the sovereign, the other being the current period when higher, benign growth is largely domestically driven and macros remain hygienic though rupee is still depreciating, according to SBI Ecowrap.

In 2013, exchange rate was uber volatile, and RBI announced a slew of measures to restore stability in foreign exchange market, notably the FCNR(B) window. However, the present scenario is different from earlier periods of crisis.

“So, by looking at the present parameters, any overseas channeled debt mop-up does not look desirable at present in particular given the decoupling of yields in DMs from the benchmark funding rates which can significantly distort the borrowing costs or desired yield on such funds sought by the NRIs/ ex-pat community. Plus, the cost of hedging such exposures can be huge,” says Dr. Soumya Kanti Ghosh, Group Chief Economic Adviser, State Bank of India.

What are the measures that can be taken under the current circumstances?

Firstly, we have adequate fx reserves of more than 10 months of imports. Short term debt to reserves is also less than 20% (of fx reserves). Meanwhile, volatile capital flows is at 64.5% (of fx reserves). These numbers by any stress of imagination are significantly comfortable. The $700 bn plus external reserve, we believe, is sufficiently strong to deter speculative moves by intervening in the foreign exchange market to prop up the rupee. There is no reason to suggest that we should use fx reserves for rainy days only as being mentioned hitherto and we believe there is still time to intervene in the market to prop up the rupee if it is so desirable.

Secondly, OMCs need to be offered a special window by the regulator that separates their daily demand (around $250-300 mn) from the market chores (annualized $75-$80 bn demand could be taken out) . This should allow better visibility on genuine fx demand and supply dynamics and in measuring the efficacy of various counter measures initiated by the regulator to curb unwarranted volatility.

Thirdly, the attempt to rationalize the open position for banks by the RBI though useful is likely to have created a significant divergence of the Onshore and Offshore markets. Indian banks (both PSBs and PVBs) are generally long onshore and short offshore, while foreign banks exhibit a contra trend. As banks attempt to unwind their positions, liquidity shortages are likely to emerge, creating a vicious cycle where offshore premiums could witness sharp rise. Thus, the NDF premia for 1 year has shot today to 4.19% (from 3.43% yesterday) while 1 month premia spiked from 0.33% to 0.67%, and the NDF /Offshore rates were quoting at Rs 98.41 today, we believe the $100 mn limit should be imposed on the trading book only and not on whole bank book level as it creates operational challenges. This is also important as many FPIs and some FDI players would be taking out their funds in present situation (reallocation / profit booking) and would be placing genuine demands on banks to fulfil on order matching basis.

Fourthly, given much of the pressure on the rupee can have a two-way pass through the debt markets, the regulator needs to concomitantly explore the probability of conducting Operation Twist that pushes up the short-term yield while sobering the yield on long term papers ensuring various reference rates remain within the prescribed bands, aligned with policy rate in calibrated manners. We also believe liquidity could be simultaneously modulated to ensure rupee also gets support.

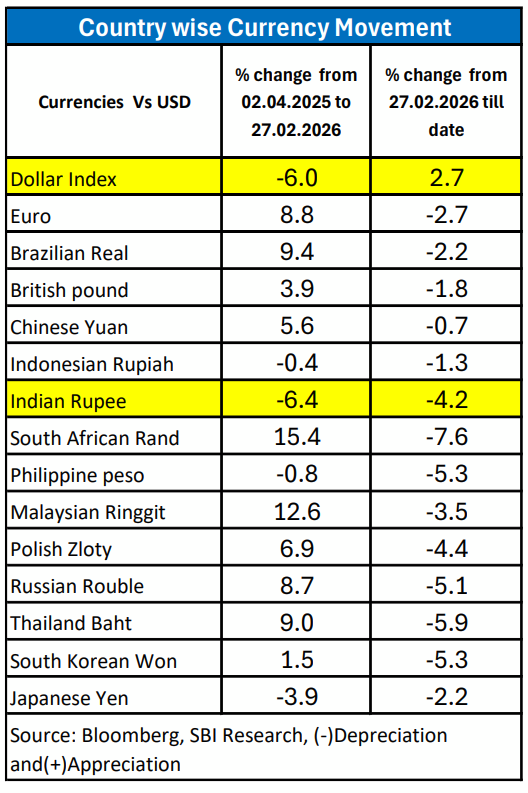

Interestingly, the Indian Rupee depreciated by 6.4% between 2nd Apr’25 to 27th Feb’26 (period 1 /the war started on 28th Feb). At the same time the dollar index also depreciated by 6% during the same period. This was the time when most currencies were appreciating against the dollar but not the rupee and thus perhaps the argument of using rupee as a shock absorber may have been overblown. The rupee depreciation post 27th Feb (period 2) is in fact in line with other currencies, and in fact better than currencies which appreciated significantly in period 1 indicating that in an uncertain world pushing the limits on rupee depreciation as a shock absorber does not hold beyond an inflection point.