India-US trade deal restores export competitiveness, yet China risk clouds the outlook

Increased imports from China, due to higher US tariffs, and global market competitiveness may suppress realisations in segments, namely chemicals and petrochemicals, limiting benefits.

Stability in US tariff policies across markets would be key to restoring confidence in investments. (Image: AI Generated)

The recently-announced India-US trade deal eliminates India’s relative disadvantage to its South-East Asian peers in exporting to the US, according to India Ratings and Research (Ind-Ra). This is likely to bolster the credit profiles of textile, chemicals, shrimp, and gems and jewellery players by enhancing margins and liquidity. With the peak Christmas demand season over and potentially slower global growth in 2026, some benefits may be spread out, necessitating interim support for affected players lower down the credit curve.

Furthermore, increased imports from China, due to higher US tariffs, and global market competitiveness may suppress realisations in segments, namely chemicals and petrochemicals, limiting benefits. However, tariff reductions can boost volume growth and support margins for those previously absorbing high tariffs. Continuing US trade policy uncertainty and frequent changes, even after trade deals, may cause volatility in both trade and capital market sentiments. Consequently, companies across sectors are likely to tread with caution in investments.

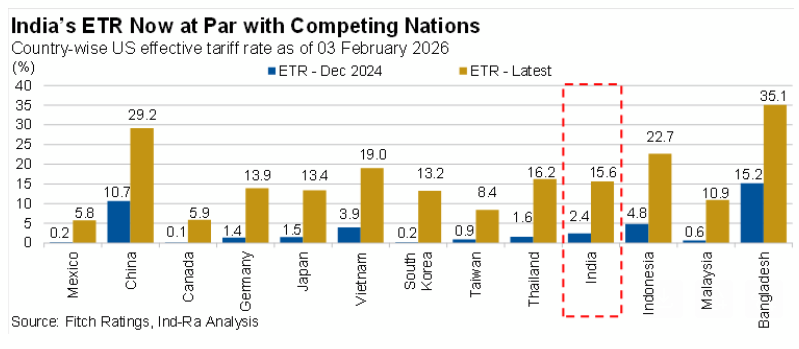

However, the effective tariff rate (ETR) after this announcement stands at 15.6% compared to 2.4% in 2024, as higher sector-specific tariff rates. China’s ETR stands at 29.2% (Source: Fitch Ratings Ltd).

“The India-US trade deal restores the relative competitiveness of Indian exports to the US from South-East Asian peers. The tariffs on China remain significantly higher. The potential for rerouting exports to markets such as India and competing with Indian exports in the global market, which is likely to slow down in 2026, however could limit the benefits in the short term. Stability in US tariff policies across markets would be key to restoring confidence in investments”, says Rakesh Valecha, Senior Director, Core Analytical Group.

Rate Sentiment Turns Cautiously Constructive: The brief US tariff announcement has offered some long‑awaited clarity to market sentiment. Persistent geopolitical risks and prolonged tariff overhang have weighed on domestic markets and the Rupee, although a detailed notification should provide further visibility. In the bond market, heavy remains the key headwind. While stronger capital inflows could help ease pressure and support sentiment, they may also reduce the immediate need for the Reserve Bank of India’s open market operation purchases in the near term.

Given the evolving dynamics of US tariff policy and subsequent global trade policy, the ongoing tariff war is no longer isolated to one‑off actions. Because any deal with one nation invariably alters the incentives and strategies of other players, tariff decisions have effectively become part of a continuous, multi‑player strategic game with shifting payoffs. As a result, market sentiment is likely to remain cautiously optimistic in the near term. That being said, Ind‑Ra assesses that the latest tariff action by the US is sentimentally positive for rates.

Sectoral Impact

Textiles: The revision in US tariffs to 18% will likely benefit Indian textile players, particularly apparel and home textiles, as India’s effective tariff will be slightly better than other competing nations and will have advantage over China (29%, largest exporter of textile to US) as well as Bangladesh (35%). The reduction in US tariff along with India’s trade deals with other key importing nations, namely the United Kingdom, European Union (EU), and United Arab Emirates (UAE) will provide tailwind to India’s textile exports. Ind-Ra believes industry players will be required to take up incremental capex for meeting additional demand from recently concluded deals; however, US trade policy uncertainty may keep corporates cautious in investments.

The US is the primary export market for the Indian textile industry, contributing around 29% to all textile exports, followed by EU at around 19%. On the other hand, India accounts for around 9% of all US textile imports, being the third-largest export market for the US, highlighting its importance as a key trade partner and provides scope to increase its share.

India’s export to the US has declined 2.7% yoy during 8MFY26, despite a 5% yoy increase in 5MFY26 before the 50% reciprocal tariffs were implemented. This decline followed due to 17% yoy growth during September-November 2025 after the 50% tariff was imposed on 27 August 2025.

Chemicals: The US is India’s largest chemical export destination, accounting for 14% of India’s chemical exports in 8MFY26. Organic chemicals accounted for around 40% of India’s exports to the US while agrochemicals constituted another 20%, including the exempt chemicals under the US executive order. While the tariffs remain higher than the pre-liberation rates, Ind-Ra believes the higher tariffs on key competitor China will enhance the competitiveness of Indian chemical exporters, allowing them to increase their US market share. The tariff ceiling on the EU, another key competitor, is slightly lower, but production costs in the region are higher. Other key competitors exporting to the US include Canada and Mexico.

Ind-Ra believes Indian players already supplying to US-based customers stand to benefit in the near term, with a likely recovery in volumes and EBITDA margins, as they had been absorbing a part of the increased cost for customers. On the flip side, India’s growing domestic demand amid global overcapacity keeps it remains exposed to the risk of an influx of goods, especially from China, affecting realisations. Ind-Ra opines that the vastly different dynamics of various chemicals will lead to a varying impact across the sector. Most Indian chemical players have witnessed volume growth in the past few quarters, even as prices remained subdued. Ind-Ra does not expect an immediate impact on the investments in the sector, as companies remain cautious given the dynamic geo-political situation.

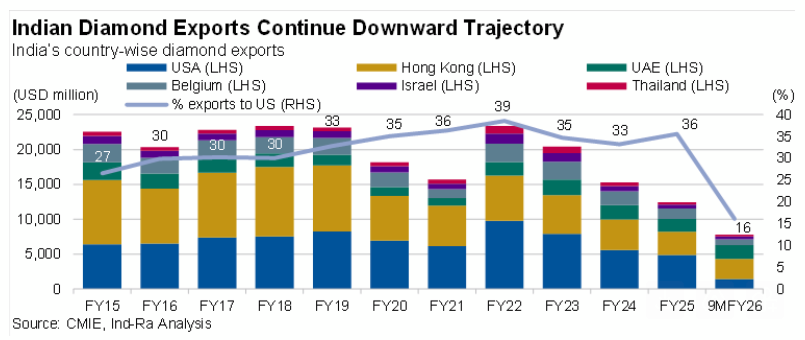

Gems and Jewellery: Ind-Ra expects some relief for the cut and polished diamond (CPD) industry, which has been under pressure due to competition from lab-grown diamonds and sluggish demand from the US and China. The tepid demand environment, due to the weak consumption trends and increased costs to US consumers due to tariffs, resulted in the total CPD exports from India dipping 7.5% to USD8,990 million in 9MFY26. Also, India’s CPD exports to the US saw a sharp decline of nearly 60% to USD1,450 million in 9MFY26, however it was largely offset by exports to major diamond trading hubs such as Hong Kong, the UAE, Belgium, and Israel, apart from an increase in domestic sales. Lower tariffs and potential demand recovery are expected to support CPD players’ margins and alleviate working capital pressures, thus supporting their credit metrics.

Shrimp Industry: Ind-Ra opines the Indian processed shrimp industry will materially benefit from the India-US trade deal through better cost competitiveness against peers namely Ecuador, Vietnam, and Indonesia, helping improve US export demand and revenue visibility. The US is India’s most critical market for frozen shrimp, representing 41% of the export volume and 48% of the export value in FY25. US exports, which had witnessed steady growth pre-tariff imposition, significantly slowed down during August to November 2025, with recovery expected from the lower tariffs.

Ind-Ra expects the financials of shrimp processing industry to come in better than the previously estimated revenue decline of 12% yoy and margins compression of 150bp yoy in FY26. Working capital pressures are also expected to be lessen with better order visibility, resulting in credit metrics falling in line with FY25 trends.

Deal Restores Relative Competitiveness: Under the revised reciprocal tariff rate of 18% (ETR of 16%), Indian goods now face lower tariffs than competitors such as Bangladesh, Vietnam, Sri Lanka, Pakistan, and Indonesia, who previously enjoyed lower effective rates. Industries such as textiles and chemicals that face high cross-price elasticity in global trade are likely to be the biggest beneficiaries of the lower relative tariffs. The deal opens up a significant gap in effective rates relative to China (29%), which may accelerate “China+1” sourcing strategies and diversification of supply chains.