Union Budget 2026 balances capex push with fiscal discipline: Ind-Ra

The union government’s focus on fiscal consolidation has established fiscal credibility among investors and stakeholders over the years.

The budget effectively balanced the capex pedal with reforms momentum to push productivity, scale-up manufacturing, enhance logistics efficiency, and human capital amid a tightened fiscal space. (Image: AI Generated)

India Ratings and Research (Ind-Ra) believes the FY27 Union Budget was presented against a backdrop of resilient GDP growth and global economic uncertainty. “The budget effectively balanced the capex pedal with reforms momentum to push productivity, scale-up manufacturing, enhance logistics efficiency, and human capital amid a tightened fiscal space. The global order has changed dynamically in the past couple of years, with tariffs being the mainstay to align countries. This along with the improved potential growth highlighted in the Economic Survey 2025-26 were the core themes for the FY27 budget,” says Dr. Devendra Kumar Pant, Chief Economist and Head Public Finance, Ind-Ra.

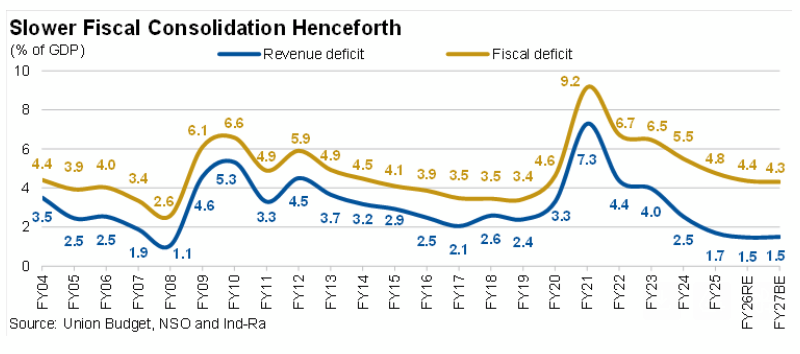

The Union government’s focus on fiscal consolidation has established fiscal credibility among investors and stakeholders over the years. “However, the fiscal deficit has been lowered by 5bp to 4.3% of GDP for FY27, marking the slowest reduction since FY19 (2bp). This is due to slowing revenues from short-term impacts of tax reforms introduced in FY26. Nevertheless, with low inflation, this will boost the economy in FY27, which we expect to grow at 6.9%”, says Paras Jasrai, Economist and Associate Director, Ind-Ra.

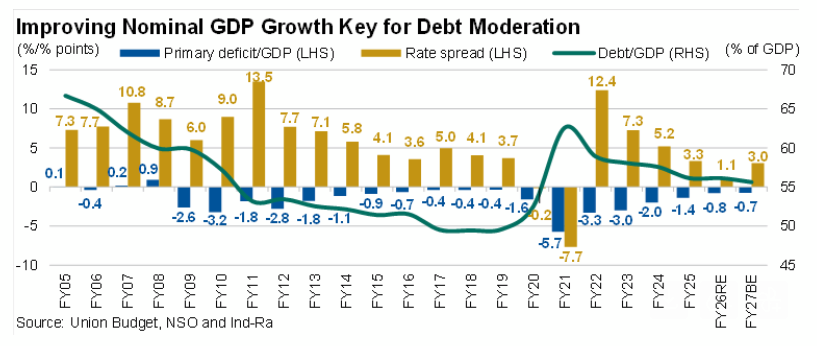

The new fiscal anchor namely, the debt/GDP ratio, is budgeted to fall to a seven-year low of 55.6% in FY27 from 56.1% in FY26 (RE). Reducing debt is crucial for the Indian economy as it provides fiscal legroom during crisis situations, as around 40% of the revenue receipts are committed to servicing previous year’s debt (interest payments) in FY27 (BE). This remains at a six-year high, significantly above the FY16-FY20 average of 36.5%. Lower leverage makes way for expenditure channelisation towards development purposes as against committed expenditure. The debt/GDP is targeted by the government to decline to 49%-51% by FY31.\

Key Themes of FY27 Budget: After boosting demand in the previous year’s budget amid slowing GDP growth, the union government has shifted its focus on enhancing the long-term productivity and competitiveness of the Indian economy against a turbulent external economic environment. Facing the highest tariffs levied by the US globally, the government in concentrating on scaling up manufacturing, supporting “Champion MSMEs”, improving infrastructure, ensuring energy security, and creating “City Economic Regions”.

For manufacturing, the government aims to address three key constraints: (i) import dependence on strategic inputs (rare earths, chemicals), (ii) limited depth in domestic capital goods, and (iii) the need to expand labour-intensive manufacturing. Key measures announced in the speech include:

Biopharma SHAKTI: INR100 billion over five years to build three new/expanded National Institutes of Pharmaceutical Education and Research (NIPERs), establish clinical trial sites, and strengthen the regulatory system

India Semiconductor Mission (ISM) 2.0: Focus on building equipment/materials, full-stack IP, supply chains, and workforce

Electronics Components Manufacturing Scheme: Proposed outlay increase to INR400 billion from INR229.2 billion since its launch in April 2025

Rare Earth Corridors in mineral-rich states

Chemical Parks: Support for three cluster-based plug-and-play parks

Capital Goods and Logistics: Initiatives include hi-tech tool rooms, a construction & infra equipment scheme, and an INR100 billion scheme for container manufacturing over five years

Textiles: An integrated programme covering fibres, cluster modernisation, handloom/handicraft integration, sustainable textiles, and skilling through Samarth 2.0, plus mega textile parks.

While the measures are growth enhancing, the success depends on state-level clearances for land and other aspects, and execution discipline. The impact of these measures is unlikely to be visible in FY27.

The capex thrust has been a clear lever in the post-pandemic era, and the union government has announced key measures: new dedicated freight corridors; operationalising 20 new national waterways over five years; a coastal cargo promotion scheme to increase waterways/coastal share to 12% by 2047 from 6%, and seven high-speed rail corridors as “growth connectors”.

The new measure to address urbanisation is the introduction of the City Economic Regions (CERs) as a spatial growth tool to help Tier II/III cities become agglomeration engines. The budget proposes mapping CERs and allocating INR50 billion per CER over five years through a reform-cum-results financing mechanism.

The employment-intensive tourism sector saw a variety of measures such as set up a National Institute of Hospitality by upgrading the existing National Council for Hotel Management and Catering Technology, a pilot scheme for upskilling 10,000 guides in 20 iconic tourist sites, set up of a National Destination Digital Knowledge Grid to digitally document all places of significance for boosting employment.

For health sectors, the budget proposed to add 100,000 allied health professionals over five years; training 1.5 lakh caregivers in the coming year; setting up NIMHANS-2 and upgrading institutes; establishing emergency and trauma care centres with 50% capacity enhancement in district hospitals; and launching five regional medical hubs for medical value tourism. There were other measures as well for supporting the fisheries sector along with a coconut promotion scheme and setting up of women enterprise retail through SHE-Marts.

To further up the deregulation and for reduction of compliance burden of the economy, the budget announced the setting up of a high-level committee on banking for Viksit Bharat, a comprehensive review of the foreign exchange management (non-debt instruments) rules, and setting up of high-powered ‘Education to Employment and Enterprise’ standing committee to focus on the services sector as a core driver of Viksit Bharat.

Realistic GDP Growth Assumption: At the core of FY27 budget is a nominal GDP growth rate of 10.0% (30bp higher than Ind-Ra’s assessment) as against 8.0% in FY26 (RE). The Economic Survey 2025-26 has pegged the FY27 real GDP growth in the range of 6.8%-7.2%, translating in a GDP deflator growth rate of 2.8%-3.2%. While Ind-Ra expects both retail inflation and wholesale inflation to pick up in FY27 after multi-year low levels in FY26, it might remain benign. Deflator growth during FY23-FY26 was 3.0%. Thus, the nominal GDP growth in the FY27 budget appears reasonable. The risk to nominal GDP growth originates only from the real GDP growth due to any escalation in the tariff war, and any capital outflow, if the dollar continues to strengthen. The new GDP series will be available from end-February 2026, and the 10% nominal GDP growth in FY27 will be reassessed accordingly.

Gross Tax/GDP Ratio Lowest in Past Six Years: Gross tax revenue/GDP (11.2%) and net tax revenue/GDP (7.3%) are budgeted to be at the lowest levels in the past six years in FY27. The net tax/GDP ratio during FY22-FY26RE averaged around 7.6%. The GST rationalisation announced in mid-FY26 and income tax exemptions in the FY26 budget have led to a declining tax ratio. However, an improving tax base in the ensuing years and improving potential growth of the economy as articulated in the Economic Survey 2025-26 may help the net tax collection/GDP to swing up.

Gross Tax Revenue Assumptions Broadly Seem Plausible: Ind-Ra believes the FY27 fiscal arithmetic looks realistic. The crux of the FY27 revenue estimates lies in the gross tax buoyancy of 0.8x (8.0% gross tax revenue growth and nominal GDP growth of 10.0%), which prima facie, appears plausible, considering 1.0x average buoyancy during FY23-FY26. While the assumed buoyancies of income tax (IT) and union excise duty (UED) in FY27 (BE) are higher than FY26, the same for corporation tax (CT), custom duty (CUST), and goods and service tax (GST) are lower. IT buoyancy was impacted in FY26 due to the IT relief provided in the FY26 budget, leading to higher buoyancy in FY27. The higher buoyancy of UED is mainly due to the expectations of stable consumption of petroleum products and increased excise duty on tobacco products from 1 February 2026. Indian has signed four free-trade agreements (FTAs) in FY26 and is negotiating FTAs with several countries. The lower buoyancy CUST suggests realistic assumption in budget preparation. The continuation of growth momentum in FY27 from FY26 and government focus on manufacturing might translate CT buoyancy at 1.1x in FY27 (FY26 (RE): 1.55x). The GST buoyancy appears to be understated (FY27: negative 0.26x, FY26 (RE): 0.24x). The GST compensation cess was discontinued from 22 September 2025; excluding GST compensation cess, the assumed GST buoyancy in FY27 is 0.63x (FY26: 0.28x). Thus, there is scope of collecting higher central GST collections in FY27. GST collection is assumed to grow 6.3% in FY27; in January 2026, the gross and net GST collection grew 6.2% and 7.6% yoy, respectively.

Non-tax Revenue Assumptions Appear to be Pessimistic: Non-tax revenue is budgeted to decline 0.2% in FY27 (BE) (FY26 (RE): 24.4%). More importantly, dividends from banks, financial institutions and the Reserve Bank of India (RBI), which is 45.6% of non-tax revenue in FY26 (RE), are budgeted to grow 3.7% in FY27 (FY26 (BE): 9.3%, FY26 (RE): 30.0%). The RBI’s proportion in the central government securities increased to 13.25% in end-September 2025 from 12.78% in March 2025, with more open market operations (OMOs) in the rest of FY26; it might increase in FY27. This is likely to translate in a higher RBI dividend to the government. India’s holding on US securities as on 31 October 2025 declined around 21% yoy; however, the 4.1% depreciation of Indian rupee in relation to the US dollar in 9MFY26 will limit the RBI’s earnings from interest from US treasuries.

The actual accrual from disinvestment receipts was just 40.7% of the budgeted level during FY20-FY25. In fact, in FY26 (RE) was 34.4% of the budgeted levels. Looking at the recent disinvestment performance, there could be some slippages in disinvestment receipts.

Quality of Expenditure Remains Robust, Revenue Expenditure at a 43-year Low: The expenditure assumptions appear plausible. As expected, the government has continued following a tighter fiscal policy in FY27 as well. The total expenditure/GDP ratio is proposed to decline to 13.6% in FY27 (BE) from 13.9% in FY26 (RE), at a seven-year low. Going by the past year trends, the government is pruning its expenditure/GDP (FY26 (BE): 14.2%; FY25: 14.1% from 14.6% in FY25 (RE)), which is expected to be the case in FY27 as well. Hence, the quality of expenditure remains robust, with the proportion of capex in total expenditure is budgeted to increase to a 23-year high of 22.8% in FY27 (FY26 (RE): 22.1%; FY04: 23.2%). The capex/GDP ratio is budgeted at 3.1% in FY27 (BE) (FY26 (RE): 3.1%, FY25: 3.2%). The capex is budgeted to grow 11.5% in FY27; in FY26 (RE), capex was 2.3% lower than FY26 (BE). As in the past, in case of slower revenue growth, the capex can be squeezed to meet fiscal deficit targets.

The revenue expenditure/GDP is budgeted at a 43-year low of 10.5% of GDP in FY27 (FY84: 9.9%; FY26 (RE): 10.8%). Revenue expenditure growth in FY27 (BE) at 6.6% was lower than last year. The proportion of committed expenditure (salary, pension, subsidy and interest payments) in the current expenditure is budgeted to decrease to 61.1% in FY27 (FY26 (RE): 61.6%, FY25: 59.6%). The committed expenditure is budgeted to grow at 5.8% in FY27 (FY26 (RE): 11.0%, FY26 (BE): 7.3%). Revenue expenditure excluding interest payment, pension, salaries and subsidies is budgeted to grow 7.9% in FY27 (FY26 (RE): 2.2%, FY26 (BE): 5.7%, FY25: negative 0.2%). Revenue expenditure arithmetic is contingent on 3.1% decline in subsidies in FY27 (BE); in FY26 (BE), subsidies were budgeted to grow at 0.9%, whereas in FY26 (RE) the growth was 11.1%.

Y26 Fiscal Correction due to Curbing of Expenditure: The FY26 revised estimates peg fiscal deficit at INR15,585 billion (4.4% of GDP) as against INR15,689 billion (4.4%) in FY26 (BE). The correction in fiscal deficit was led by lower expenditure in RE than budgeted due to a lower mop-up in revenue receipts. The FY27 (BE) fiscal deficit is proposed at 4.3% of GDP, which was higher than Ind-Ra’s assessment.

OMOs and Security Mix Key for Market Interest Rate: G‑Secs and state government securities continue to weigh on market sentiments and pressure from large and higher duration supply dampening the transmission of monetary policy. With net borrowing projected at INR11.7 trillion, participants will keenly watch for sizeable OMOs and security mix in the upcoming issuance calendar. Ind-Ra has already underscored that the scope for further monetary transmission remains limited in FY27, as highlighted in its FY27 Credit Market Outlook. On the shorter end, the elevated T‑bill supply may exert additional pressure, though abundant liquidity and stable policy rates should provide some buffer. The renewed push toward deepening the corporate bond market and advancing total return swaps (TRS) is a constructive step, but these remain medium‑term reforms. Also, TRS will require a more supportive tax framework to truly scale. Likewise, the securitisation of micro, small and medium enterprises’ (MSMEs) receivables is a welcome initiative, especially with elevated loan-deposit ratios and banks facing constraints from sluggish deposit inflows. TRS stands well‑positioned to add meaningful support, but its real success will hinge on a tax framework that aligns with investor expectations. The domestic securitisation market has already been gathering steady momentum, supported by regular issuance activity from non-banking finance companies. With a conducive tax regime, MSME‑receivable securitisation could emerge as an attractive avenue for domestic credit funds, unlocking deeper participation and accelerating market development.