Affordable housing lenders set to sustain 19-20% AUM growth over next two years: Crisil Ratings

Growth will be driven by strong demand from Tier 2 and smaller cities, steady home loan expansion and robust loans against property (LAP) disbursements, despite global uncertainties and a slowdown in affordable housing launches in metros.

Macro fundamentals remain supportive for steady growth in the AUM of A-HFCs, underpinned by rising urbanisation, favourable demographics and low mortgage penetration. (AI Image)

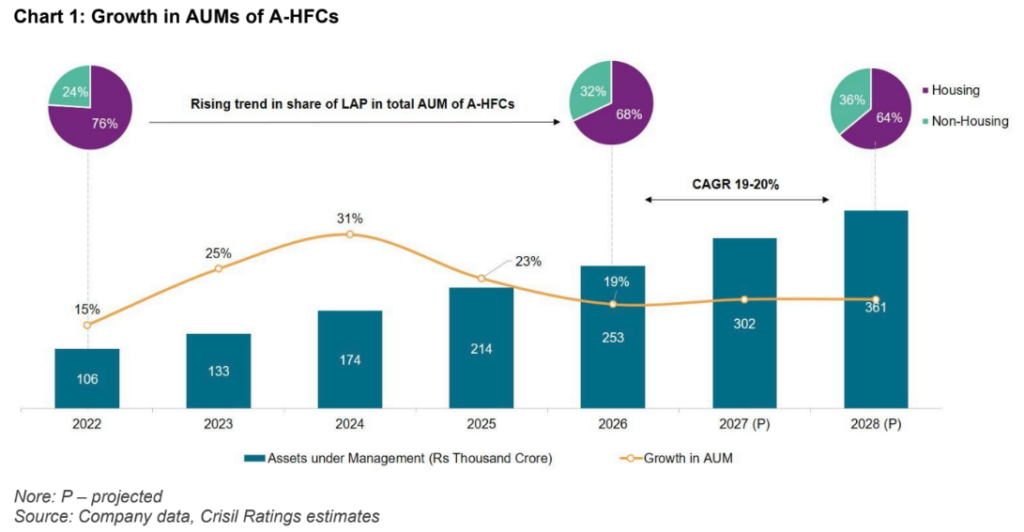

Growth in assets under management (AUM) of affordable housing finance companies (A-HFCs) is expected to remain healthy at 19-20% this fiscal and the next, in line with the ~19% growth last fiscal, according to Crisil Ratings.

Home loans, which account for ~68% of AUM are expected to grow at 17-18% in fiscals 2027 and 2028. Loans against property (LAP), the other major business, should grow faster at ~23% over the same periods even as lenders strengthen underwriting in some borrower cohorts.

Macro fundamentals remain supportive for steady growth in the AUM of A-HFCs, underpinned by rising urbanisation, favourable demographics and low mortgage penetration. Affordability, derived from the triad of income growth, house prices and interest rates, has also improved in recent years as income growth outpaced property prices2.

Says Subha Sri Narayanan, Director, Crisil Ratings, “While headline data points to a moderation in launches and sales of affordable housing projects, this largely pertains to metros and is unlikely to materially affect the growth trajectory of A-HFCs for two reasons. One, their portfolios are structurally skewed towards the Tier 2 and smaller markets, which account for over 75% of industry-wide3 loans below Rs 35 lakh4. Two, ~45% of the lending by A-HFCs is directed towards self-construction and resale of houses, segments that are not dependent on new project launches.”

Demand in the Tier 2 and smaller markets will also get a leg-up from India’s economic growth, the ongoing infrastructure buildout and sustained government support, reinforcing the long-term prospects for A-HFCs.

LAP, which galloped at a CAGR of ~37% between fiscals 2023 and 2025, is expected to continue outstripping growth in home loans, albeit at a more measured pace than before.

Strong demand from micro, small and medium enterprises (MSMEs) has helped this segment, while improved access to borrower data, greater use of analytics and stronger underwriting frameworks supported portfolio expansion.

The higher yields are attractive to lenders trying to protect margins amid intensifying competition. However, they have curtailed disbursements to the sub-Rs 10 lakh segments last fiscal amid elevated borrower leverage and spillover of stress from microfinance cohorts, leading to slower growth in those categories.

Says Aesha Maru, Associate Director, Crisil Ratings, “Over this and next fiscals, LAP is expected to grow at ~23%, nearly in line with the ~24-25% last fiscal. This reflects the cautious stance adopted by lenders in certain lower-ticket borrower segments to manage the potential stress there. In addition, heightened global uncertainties and uptick in inflation stemming from the conflict in West Asia, and their potential impact on borrower cash flows, could further temper risk appetite in the near term, leading to tighter credit filters and selective disbursements.”

Nevertheless, continued demand for both affordable housing and MSME financing, supported by prudent underwriting and stronger risk controls, should help A-HFCs sustain healthy portfolio growth and controlled asset quality metrics.

Any sustained uptick in interest rates and other macro headwinds bear watching in the road ahead