West Asia supply shock may push aluminium EBITDA above $1,450 per tonne

Cost efficiencies of domestic producers will be underpinned by highly integrated operations, including captive power, alumina refinery, and bauxite linkages.

Elevated prices due to global supply deficit, along with cost competitiveness, will support cash accruals. (AI Image)

A global aluminium supply deficit, triggered by the West Asia conflict, is poised to drive aluminium prices to record highs, improving realizations for Indian primary aluminium manufacturers. This, along with contained cost of production, is likely to uplift profitability of players to a decadal high of above $1,450 Ebitda per tonne in fiscal 2027, according to Crisil Ratings.

Cost efficiencies of domestic producers will be underpinned by highly integrated operations, including captive power, alumina refinery, and bauxite linkages. These factors, along with healthy capacity utilization, will lead to robust cash accruals and keep credit profiles strong.

Our study of three domestic primary aluminium producers — accounting for ~90% of India’s 4.6 million tonne (MT) capacity— indicates as much.

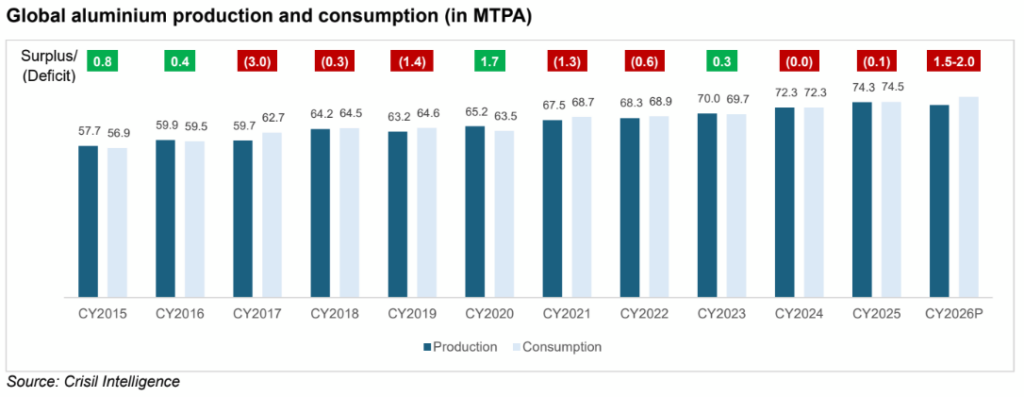

The global supply deficit has been triggered by production curtailments across the Gulf Cooperation Council (GCC) region, which accounted for 8.3% of global aluminium production in calendar year 2025. Strikes on critical smelting infrastructure, compounded by gas supply shortages, have disrupted GCC supply by 40–50%, which could widen the global supply deficit to a decadal high of 1.5-2.0 MT during the year.

The supply shock has translated swiftly into elevated London Metal Exchange (LME) aluminium prices, which have averaged above $3,500 per tonne, the highest in a decade, since the onset of the West Asia conflict in February 2026.

Says Ankit Hakhu, Director, Crisil Ratings, “Disruption caused by the West Asia conflict is significant, considering the global supply deficit averaged below 0.5 MT over the last 5 years. With global smelting capacities operating above 90% utilization and China’s primary output already near its 45 MT cap, there is limited room to offset the GCC shortfall, further constrained by high lead times to commence or restart fresh production. Even in a scenario of the West Asia conflict being resolved in the next one to two quarters, this deficit is likely to keep prices elevated in the range of $3,200-3,300 per tonne through fiscal 2027.”

This puts Indian primary producers in a sweet spot, as their realisations are benchmarked to LME prices, while their costs remain among the lowest globally, with the majority of smelting capacities operating in first quartile of global cost curves.

Their cost competitiveness rests on two structural pillars.

First, Indian players utilise more captive coal-based power than their global counterparts, which rely more on gas-based power. The former’s power costs, accounting for ~40-45% of total production cost, thus remain stable, supported by benign domestic coal prices amid healthy coal production in the country. Further, the power plants are co-located with their smelters, which insulates them from global gas market volatility.

Second, India has healthy domestic bauxite availability and high backward integration for alumina production to meet 85- 90% of requirements. Raw materials account for ~30-35% of total production cost, and healthy availability shields domestic producers from raw material volatility.

The remaining expenses, mainly for fixed-cost components, have lower variability than coal and alumina costs, and are expected to further support the steady cost curves for domestic players.

Consequently, the total production cost will remain relatively steady in the range of $1,900–1,950 per tonne for integrated Indian producers this fiscal, against an estimated ~$1,865 per tonne during fiscal 2026.

Says Ankush Tyagi, Director, Crisil Ratings, “The key advantage Indian producers hold in this milieu is their self-sufficiency in key raw material availability for primary aluminium production. Unlike GCC smelters, Indian players rely mainly on domestically sourced raw materials like coal and bauxite. Thus, a sharp increase in realizations will push operating margins of Indian primary aluminium producers above $1,400-1,500 per tonne this fiscal — well above the decadal average of ~$560 per tonne.”

The boost in operating margins comes at a time when domestic producers have expanded their capacity to meet the buoyant domestic demand, which is expected to grow ~7-9% this fiscal driven by increasing electrification and electric vehicle (EV) adoption. Furthermore, export opportunities may also improve, particularly from buyers in Europe, Japan, and the US, who previously sourced from GCC suppliers.

Thus, despite a rise in domestic capacity, these factors will support healthy utilization levels of 85-90%.

As a result, operating cash accruals are also expected to reach a decadal high this fiscal, and will keep credit profiles strong, with net leverage expected to remain below 2.0 times.

That said, faster-than-expected GCC capacity restoration, resulting in a sharp unwinding of LME prices, could affect these estimates and will remain monitorable.