West Asia truce caps India Inc’s profit impact at around 100 bps: Crisil Ratings

A sustained US-Iran truce and the reopening of the Strait of Hormuz could ease input cost pressures, limiting the impact on India Inc’s operating margins to around 100 basis points this fiscal, says Crisil Ratings.

The impact on both revenue and margins will be minimal for 24 sectors, with recovery largely backloaded to the second half. (AI Image)

The reopening of the Strait of Hormuz following a tenuous US–Iran memorandum of understanding (MoU), if enduring, can materially ease the profitability pressure on India Inc for the rest of this fiscal versus what was envisaged earlier, according to Crisil Ratings.

Energy markets have responded swiftly to the respite with crude prices softening. However, the availability of crucial inputs such as gas and urea is expected to improve only gradually as structural supply-side disruptions that occurred during the conflict are sorted. At present, ships transiting the Strait number well below the pre-conflict levels.

If the truce holds and there are no further disruptions, our assessment of 34 sectors exposed to the conflict indicates the impact on operating margins will be contained at ~100 basis points2 (to ~11% this fiscal from ~12% expected prior to the conflict). Earlier, assuming a prolonged conflict and closure of the Strait, we had pencilled in an impact of 200 bps.

Says Subodh Rai, Managing Director, Crisil Ratings, “The recent sharp correction in crude oil prices and likely normalisation of gas supplies are beneficial for India Inc as that would ease cost pressures meaningfully. If the armistice sustains, two-thirds of the 34 sectors will see minimal disruption, with margin recovery in the second half mostly offsetting pressures of the first half. But the risk of conflict escalation persists, so we foresee corporate India staying cautious and continuing to focus on supply-chain diversification.”

Further, demand conditions remain underpinned by government-led infrastructure spending and expectations of steady consumption. Moreover, the calibrated price hikes undertaken to offset rising input costs should support realisations.

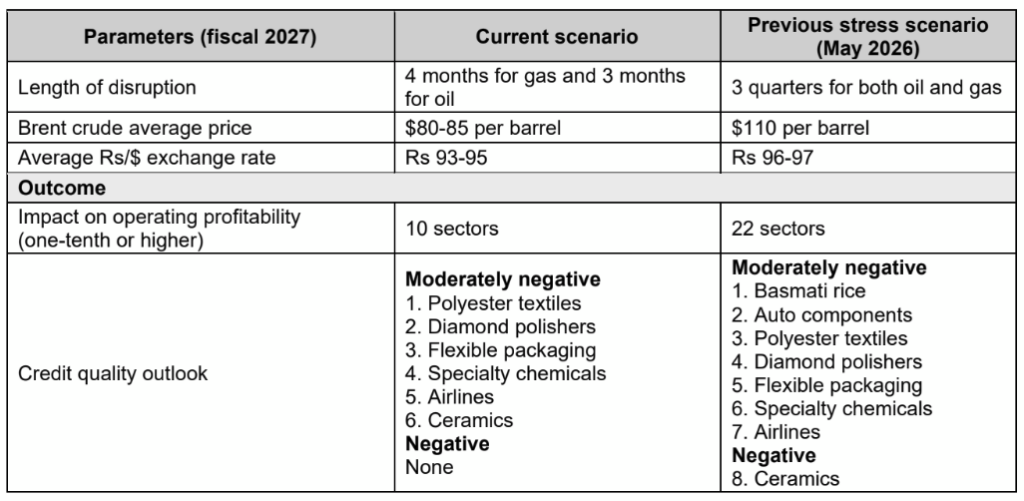

“Our analysis of 34 sectors, representing 65% of rated corporate debt, assumes crude oil supplies will normalise swiftly and the price of Brent will average $80-85 per barrel this fiscal. Gas supplies would lag a bit with overall disruption assumed at 4 months for this fiscal. The reopening of the Strait is also expected to gradually reduce India’s dependence on high-cost spot gas,” says Rai.

The impact on both revenue and margins will be minimal for 24 sectors, with recovery largely backloaded to the second half. The remaining 10 sectors face a meaningful squeeze with operating margins declining by one-tenth to one-third, compared with the pre-conflict estimates.

For four of these 10 sectors, the credit quality outlook is stable/neutral as the balance sheet strength would cushion the impact of lower profitability. Whereas for the rest six sectors, the credit quality outlook is moderately negative3 because of one-tenth or more impact on profitability, higher working capital requirement and moderate balance-sheet strength.

Airlines: First-half margin compression is unlikely to fully reverse given currency pressures, capacity rationalisation and constrained pricing power, which would strain profitability

Ceramics: Elevated fuel costs, limited gas availability and the consequent decline in capacity utilisation will compress margins in the first quarter, with only a partial and gradual recovery as supply conditions, pricing and utilisation expected to improve over the rest of this fiscal

Commodity-linked sectors (flexible packaging, specialty chemicals, polyester textiles): Elevated input costs and moderate ability to fully them pass on will weigh on margins

Diamond polishing: Persistent demand disruptions will weigh on both volume and profitability, delaying recovery

Importantly, no sector is expected to witness high impact on either revenue or profitability at this juncture

The relatively lower impact comes out in sharp relief when compared with our previously assessed stress scenario that involved a disruption of up to three quarters. As many as 22 sectors would then have seen material margin pressure— defined as one-tenth or more decline in operating profitability—and about eight sectors would have faced moderately negative, or negative credit quality outlook due to limited financial buffers.

A comparison of key assumptions and outcomes of our current and previous scenario assessments is below:

Policy support continues to provide cushion for incremental working capital requirements, particularly for the vulnerable segments. The working capital requirements are higher because of relatively longer supply-chain cycle and elevated procurement costs. The Emergency Credit Line Guarantee Scheme (ECLGS) 5.0 provides crucial cushion to MSMEs4 with additional credit flow of the Rs. 2.55 lakh crore (including Rs 5,000 crore earmarked for airlines). As of June 9, 2026, over Rs 48,000 crore of guarantees had been approved, according to the Ministry of Finance.

Among the 24 sectors expected to see minimal impact, oil marketing companies (OMCs) and fertiliser manufacturers stand out for a sharp turnround in profitability. Between March and May, net under-recoveries (after inventory gains) for OMCs are estimated at Rs 40,000–45,000 crore5. Even if excise duties were reverted to pre-conflict levels and retail fuel prices remain unchanged, OMCs are likely to report operating profits for this fiscal, offsetting earlier losses.

Similarly, the fertiliser sector, supported by priority gas allocation, is expected to see limited impact on profitability as supply conditions improve and subsidy support remains intact. The government’s fertiliser subsidy outlay is now estimated at Rs 2.4- 2.6 lakh6 crore for this fiscal, about Rs 15,000 crore lower than earlier projections that had factored in a longer period of elevated gas and crude-linked input costs stemming from supply disruptions.

Two factors temper the otherwise stable credit quality outlook for India Inc. One, the manifestation of El Niño conditions this fiscal is expected to result in below-normal rains and could also disrupt its timing and distribution posing a key risk to rural demand. Two, the US-Iran MoU is interim and non-binding, which keeps the risk of a fresh conflict high.

Says Somasekhar Vemuri, Senior Director, Crisil Ratings, “The correction in crude oil prices and the gradual easing of both shipping-related costs and gas supplies provide timely relief to India Inc. While supply-side pressures are expected to abate, the geopolitical situation in West Asia remains fluid and escalation risks persist. Nevertheless, softer crude prices would support the government’s ability to sustain its capital expenditure push and respond to any demand-side impact. This becomes particularly relevant as El Niño poses risks to the monsoon and, in turn, domestic rural demand.”