Global bond yields turn sticky amid inflation fears, India’s 10Y seen near 7%

Persistent inflation concerns, rising global yields and uncertainty over the US-Iran conflict are expected to keep India’s benchmark 10-year bond yield under upward pressure despite comfortable domestic liquidity conditions.

India’s 10Y yield is expected to remain in the range of 6.9-7.1% in the current month, with risks tilted to the upside. (AI Image)

Global yields showed considerable stickiness from fear of inflationary risks. Major central banks hinted at possibility of a rate hike in the coming months (ECB, BoJ). Inflation projections have been revised upward unanimously by majority of them, hinting at a different contour in the coming months. For China, PPI rose to its near 4-month high and more importantly, it has reversed its 41-months deflationary trend and is reporting inflation for the past two months. Thus, price side pressure is imminent across economies (PMI survey also conveyed the same), according to Bank of Baroda’s latest Bonds Wrap report.

“We expect global yields to trade with an upward bias this month as well. The narrative of a peace deal is now changing to prolonged uncertainty. With the recent reports of US rejecting Iran’s peace plan, the upside risk on yields seems to be elevated,” said Dipanwita Mazumdar, Economist, Bank of Baroda.

On the domestic front, liquidity is comfortable at ~0.8% of NDTL. Net durable liquidity has shown some moderation, and some pressure might be visible due to faster pace of accretion in currency in circulation. For India’s 10Y yield, directional convergence will be more with global yields. We expect India’s 10Y yield to trade in the range of 6.9-7.1% in the current month, with risks tilted to the upside.

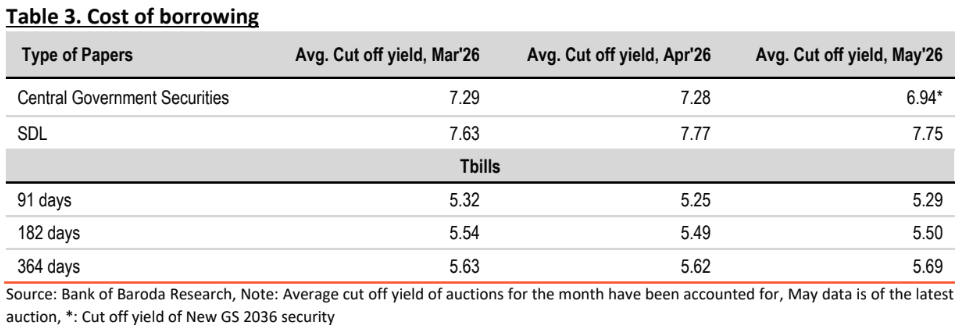

The cut-off yield for the New GS2036 at 6.94% also suggests that yield is likely to hover in that range and not expected to be much below the 6.9% mark.

Global yields showed upward bias:

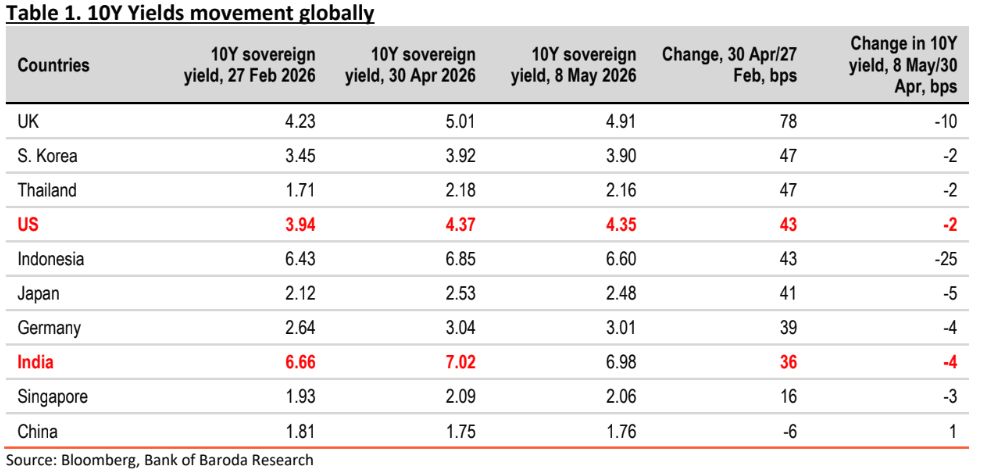

• Global yields rose sharply across the board when the change is considered from 27 Feb 2026, the start of the war. In Apr’26, UK’s 10Y yield rose at the sharpest pace followed by S. Korea, Thailand and US. Majority of the global Central Banks hinted at inflationary risks from the ongoing war. In majority of the PMI surveys for different countries, stickier input price has been flagged as a concern.

• For UK, major macro variables showed growth remaining stable such as monthly GDP, industrial production, net consumer credit and Rightmove house prices. Indicators of inflation such as retail sales, CPI and BRC sales data, remained sticky. 10Y yields have also shot up, eyeing the election and public sector net borrowing data (higher than expected in Mar’26).

Recent commentaries of central bank officials have been moderately hawkish, with Governor Bailey hinting at the need to raise interest rates in the event of continued supply side disruption from war.

• US 10Y yield rose by 43bps in Apr’26 (since 27 Feb’26). For US, there has not been much impact on growth indicators due to the war. The new home sales data remained robust, core capital goods orders improved, JOLTS job openings picked up, and non-farm payroll has beat expectations. Q1 advance estimate of GDP also improved. Price pressure persisted as reflected in the core PCE data and firming up of 1-Yr inflation expectations. CME Fed watch tool is attaching a very low probability of rate hike in H2 of CY26. But it is likely that for Fed it is going to be a pause for now.

• Germany’s 10Y yield has risen by 39bps in Apr’26 as ECB signaled higher chances of a rate hike in the next policy meet, scheduled in Jun’26. Inflation accelerated to 3%, much higher than the 2% mandate of the Central Bank. Investors have also priced in 75bps hike over the next year. Recent commentary by officials have also hinted about the tightening cycle to begin soon, especially ‘if the inflation outlook doesn’t improve significantly’.

• BoJ have hinted at possibility of rate hike in the coming months, if there is no early end to the war and inflation continues to breach central bank target levels. The central bank also revised upward its inflation projection for fiscal 2026 to 2.8% from 1.9% in Jan’26. Investors have priced in rate hike in Jun’26.

• May’26 started on a favourable note for major global yields amidst attempt to maintain ceasefire between US and Iran. However, with the latest round of developments surrounding US rejection of Iran’s peace plan, global yields might face some upside risks.

Domestic 10Y yield inched up sharply, in line with global yields in Apr’26. It traded in the range of 6.87-7.13% during the month. In May’26, however, it has shown some downward correction with the reports of war ending soon. However, any delay in formal peace deal, will continue to put upside risk on India’s yield.

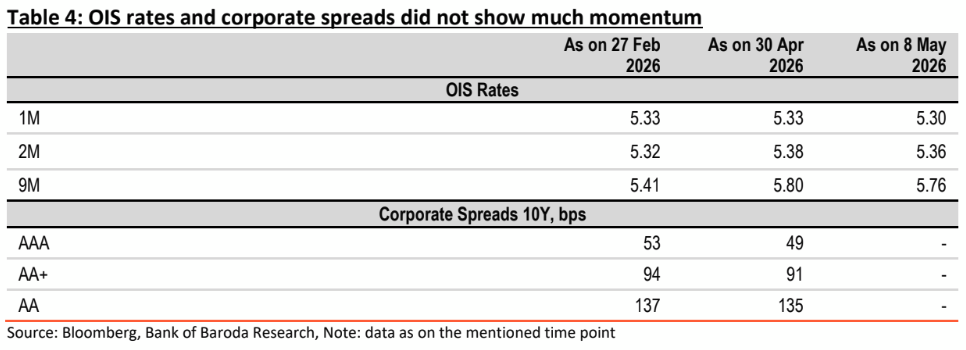

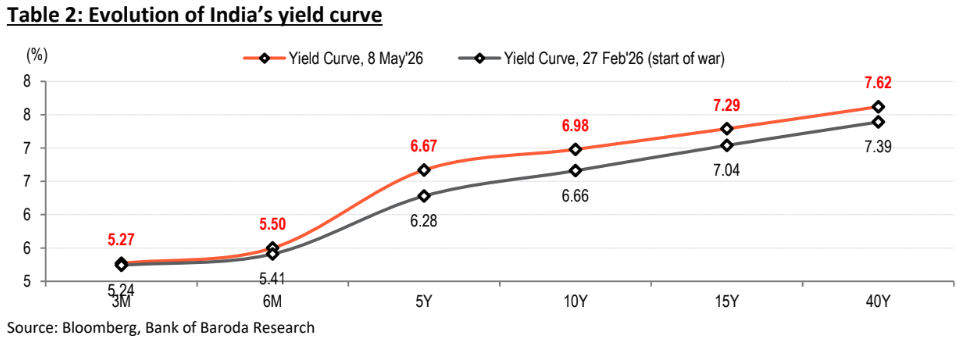

Yield curve comparison reveals that 5Y-40Y part of the curve has exhibited considerable stickiness as inflationary concerns from a rising oil price dominate investor sentiments. The gap between 10Y and 3M paper rose to 171bps as on 8 May 2026 compared to 142bps as on 27 Feb 2026. The short-end part of the curve was supported by ample system liquidity, not exhibiting much momentum. Going forward, if geopolitical risks pacify, some flatness in yield curve might be seen, else rising yield gap will continue.

What do auctions in the domestic market reflect?

In Apr’26 and May’26, cut-off yields for State government papers have inched up. For central government papers, it has remained stable. The cut off yield for May’26 is ofthe new GS 2036 security.

For T-bills cut off yield has softened in Apr’26 compared to Mar’26. However, the first auction of May’26 showed some upward momentum.

Liquidity might witness some pressure:

• Average system liquidity rose to Rs 3.4 lakh crore surplus in Apr’26 and in May’26 (average till 8th May), the surplus is Rs 2.3 lakh crore. Based on the NDTL data of 15 Apr’26, current May’26 average is at 0.8% of NDTL. The high surplus in Apr’26 may be due to possible frontloading of government spending (as there was fall in the government cash balance) and bond redemptions. The VRR auction in Apr’26 remained undersubscribed while VRRR remained oversubscribed, speaking of comfortable system liquidity.

• Net Durable liquidity has moderated to Rs 4.3 lakh crore surplus as on 15 Apr 2026 compared to Rs 5.1 lakh crore in the previous fortnight. We can expect further moderation on this front due to increase in currency in circulation. On YoY basis, CIC has been the highest since 26 Mar’21. Some leakage due to depletion in foreign exchange reserve (US$ 8bn decline in Fx reserves between 24 Apr 2026 to 1st May 2026), also needs to be watched. A lot hinges on the duration of the war and its impact on INR and foreign exchange reserves.

• Going forward, RBI’s finetuning through the LAF window would ensure that liquidity remains in the 1% NDTL surplus level.

• For the first fortnight of Apr’26, Banking liquidity (Incremental Deposits+borrowings net of incremental credit and investment, Rs lakh crore) has been at Rs 0.2 lakh crore, since it is just the start of the financial year.

Outlook on 10Y yield in the current month:

• India’s 10Y yield is expected to remain in the range of 6.9-7.1% in the current month, with risks tilted to the upside. Major risk emanates from a delay in formal peace deal which will continue to make yield sticky. The latest reports of US rejecting Iran’s peace plan, hints at higher probability of yield hovering around the 7% mark. Another key event to watch for is the India’s inflation print as market will be looking for cues of pass through of higher global prices both on producer and retail front. For CPI, any print above 4% mark, poses upside risk to yields.

• In May’26 (up to 8th May 2026), we saw net FPI debt inflows at US$ 460mn compared to net FPI equity outflow of US$ 1.5bn. However, amidst a volatile dollar and elevated geopolitical risk, pressure on debt outflows may continue to build up and it would put pressure on India’s 10Y yield.